Economic Outlook

Global economy: sitting on the fence of uncertainty

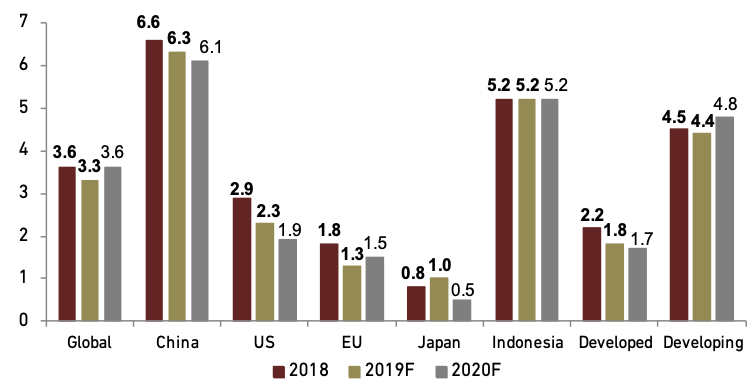

As global economic events unfold in unexpected ways in 2019, global economic downturn is inevitable. There are three major events triggering world’s uncertainty: unfavorable major events in several countries, US – China trade war, and wobbling Fed Fund Rate (FFR) movement. We predict uncertainty will stay for the rest 2019, but there is a hope for the economic downturn to recover in 2020. On Indonesia, in light of some relatively optimistic macroeconomic data, constructive sentiment seems to stay stable in 2019 and 2020. Domestic demand will still be the main driver of growth in 2020. Supported by our estimated stable inflation of 3.5%, increased investment rate to 6.1% and downward trend on unemployment among years, Indonesia’s economic growth is estimated to reach 5.1% in 2020, slightly lower compared to IMF’s 5.2% on growth of Indonesia as figured in Exhibit 1.

- Unfavorable economic major events among countries

European countries are in verge of recession like German and political instability like UK and Italy. Move to Latin America, Argentina is defaulted on its sovereign debt in August meanwhile Brazil is heading to recession. On a flip side, global demand to stay firm underpinned by easing monetary policies, low unemployment rate in both major and emerging economies, high consumer optimism in the US and China and moderate inflationary pressure.

- Breakthrough on trade war but better to batten down the hatches

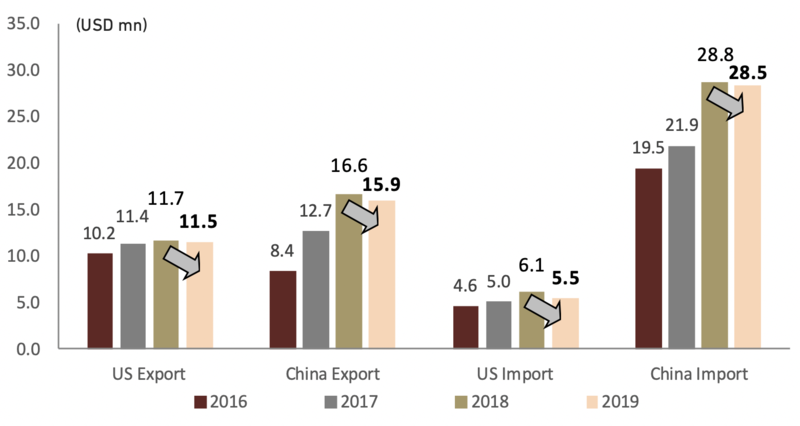

There are some multilateral disputes that could harm the already-slowing Indonesia trade performance. US-China trade war tension escalates waveringly but it seems that both sides want to keep the trade talk on tracks.. In Exhibit 2, from January to August 2019, China and US showed a 4.39% in average of the decrease among export-import to Indonesia though both of them are our 1stand 4thtop trading partners.

Exhibit 1: Global Economic Growth Forecast

Source: IMF

Exhibit 2: US and China Export-Import Performance to Indonesia

Source: Statistics Bureau (BPS)

- FFR cut for the first time in a decade

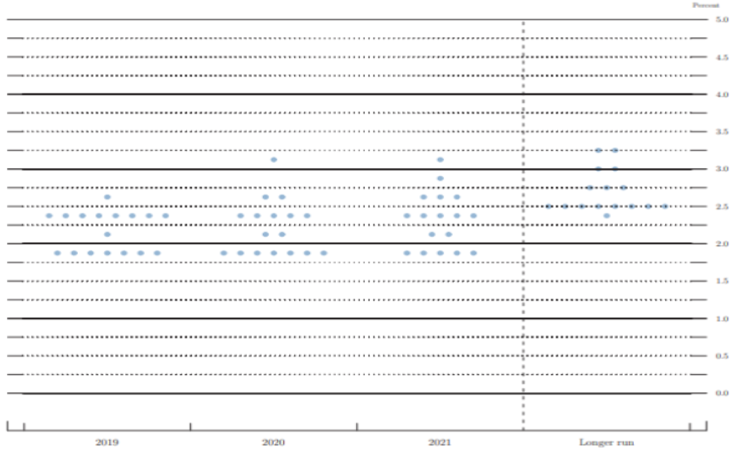

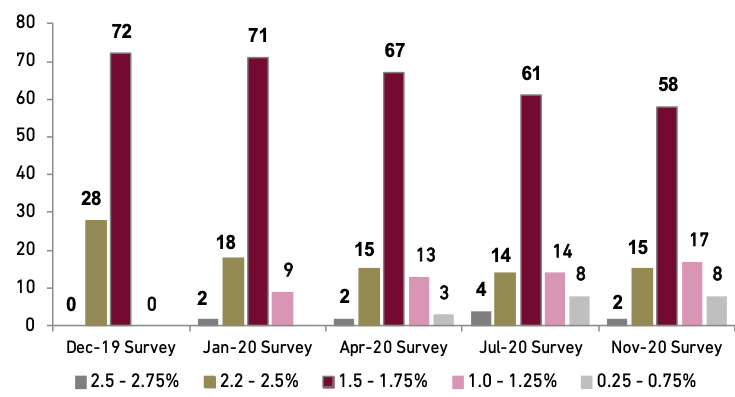

There were 2 times of FFR cut on Jul-19 and Sep-19 each from 2.25%-2.5% on Jan-19 to current level 1.75%-2.0% on Sep-19. The cut was meant to support domestic consumption amid the low inflation and disruptive US – China trade war. The rate cut was done under Trump’s pressure on Powell, the Chairman of the Fed,even Trump urged for negative FFR. Basically, Powell’s gesture indicated that the rate cut was just “mid-cycle adjustment to policy” or there would be no long series of rate cut in the near future. However, the Fed released the dot plot projection that shows an upward trend of FFR until the longer run as figured in Exhibit 3. In contrary, at end of 2019, most of economists surveyed by Bloomberg were still dovish and predicted FFR will have one more time cut until the YE 2019 as figured in Exhibit 4. From about 53 surveyed economists, 58% of them predicted FFR will be on 1.5%-1.75% until YE 2020. From the survey, we can see there is a tendency to cut the FFR lower since the number of surveyed economist from the ones who predicted FFR lower than 1.0% is likely to grow over time. We expect the rate cut would not be aggressive in 2020 or set lower by 50 bps to 1.25% - 1.5%.

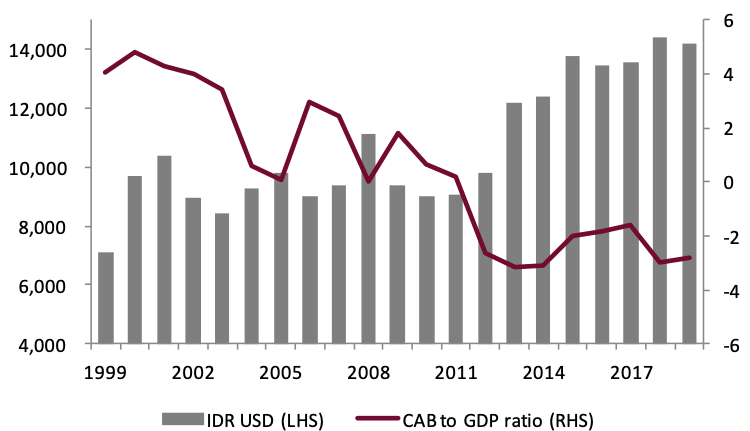

Indonesia’s CAD to slightly lower but remains manageable

Since late 2011, Indonesia started to post a current account deficit (CAD) and it has remained in deficit ever since. In 1H19, CAD was 2.82% or higher than 2.51% of CAD to GDP on 1H18. The widening CAD was driven by 2.96% increase YoY on the 1H19 of payment side on primary income account. Higher contribution of primary income account on CAD is understandable since the government has to pay dividend and interest payment as the results of investment inflows and raising debt. We predict the deficit in primary income account will be posted higher on 2H19 since there was a huge jump by 271% from USD5,280 mn in 1H18 to USD19,603 mn in 2H18 on financial account with higher contribution from the portfolio investment inflows (66% of the financial account) on 2H18 compared to the previous semester. In 2020, we see there will be a big potential on the increase in primary account deficit since we see the investment inflow will be much higher as what the government pursued all of this time. Assuming no significant changes from secondary income account, higher deficit on primary income account and better prospect ahead from the cooling trade war, we expect CAD at 2.5% of GDP 2020F, lower than 2019F at 3.0% of GDP.

Exhibit 3: FOMC Participants View on Future Monetary Policy

Source:The Fed

Exhibit 4: Bloomberg Economist Survey Estimate of 2019-2020 FFR

Source: Bloomberg

- Trade deficit lower but CAD to remain high at 3.0% of GDP

As the commodity price downtrend, trade balance will sway into deficit in 2019 and 2020 since Indonesia is net oil and gas importer but an overall net commodity exporter. We expect trade balance to remain in deficit territory but with lower magnitude from USD8.5 mn in 2019F to USD7.0 mn in 2020 of trade deficit. Moreover, due to the global downturn, the trade deficit growth trend seemed increasingas we experienced USD110.0 bn export growth and USD111.9 bnimport growth, reaching USD1.9 bnof trade deficitas of Aug-19. Lower oil price in 2019 (2019 avg: USD64.5/barrel (as of Sept) vs. 2018 avg: USD71.6/barrel) gave another challenge to trade. Even though the trade balance performance seemed better,it was due to the weaker import instead of stronger export performance.We see that Indonesia trade deficit will achieve USD7.09 bn in YE 2019 and get narrower on USD5.24 bn in YE 2020.

Indonesian government will impose export levies for CPO products and its derivatives starting January, 1st2020, delaying the prior plan in imposing levies on Nov-19. This sector got special attention from the government as it is an important foreign exchange earner while it opens more than 16.2 mn job creations. Since 2018, Indonesia implemented zero export levy for palm oil products to protect the domestic industry from falling prices due to flagging exports and oversupply. Also, the government mandated to shift to B30 in attempt to reduce the oil import gap. The B30 implementation will increase the consumption of domestic CPO. We believe implementing B30 policy and export levies will bring better outcomes. Furthermore, we see that Rupiah depreciation itself will help on reducing import next year. We expect real import to grow -2.0% YoY in 2020F from -5.5% in 2019F.

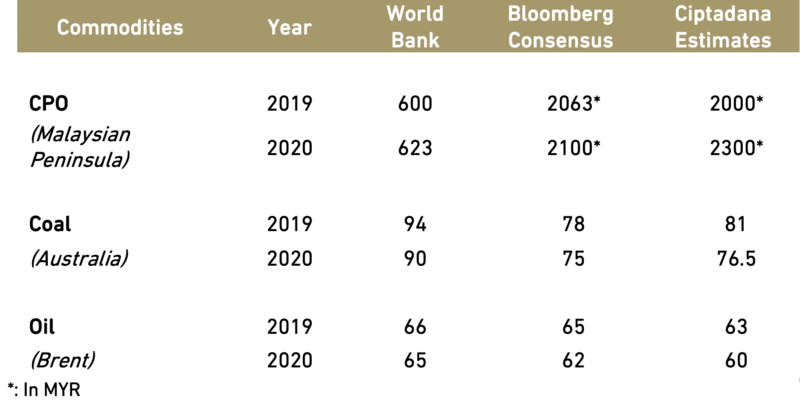

- Limited boost from commodities price

We do not expect coal and oil price to become the main driver of export growth in 2019 and forth. Asia-Pacific coal benchmark Newcastle prices is expected to average USD76.5/ton in 2020, lower from USD81/ton this year average. However we see there will be a pick up on CPO price as our analyst expect it will increase to MYR 2,300/ton. We expect real export to decline at slower pace of 1.0% YoY in 2020F from -5.0% in 2019F.

Exhibit 5: Commodities Price Forecast (Annual Average)

Source: WB, Bloomberg, Ciptadana Estimates

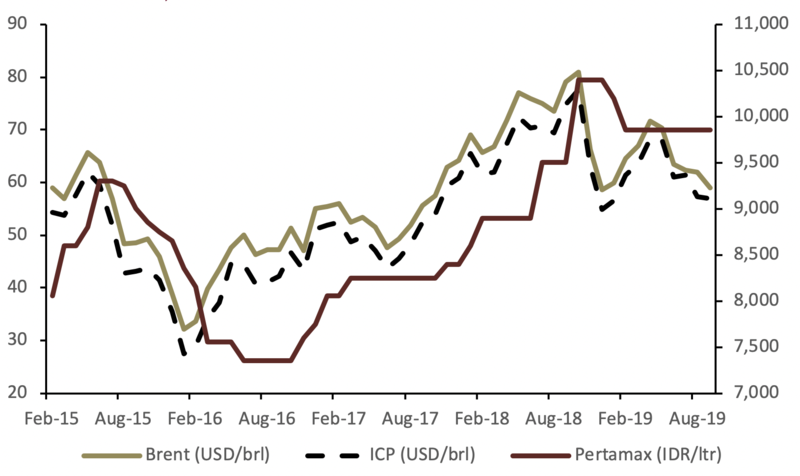

Exhibit 6: Brent Oil, ICP and Pertamax Price

Source: Bloomberg

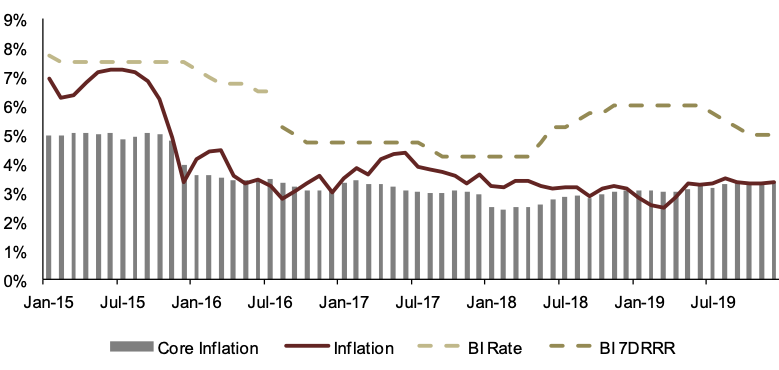

Inflation to remain stable at 3.3%

Thanks to political year that somehow correlated with the increase of subsidies in some sectors (From 2018 to 2019, fuel and electricity subsidies increased 115% YoY from Rp46.9 tn to Rp100.9 tn and 24% YoY from Rp47.7 tn to Rp59.3 tn, respectively), Indonesia can keep its inflation manageable. We remain confidence in2019 inflation will be 3.3% under BI’s 3.5±1% expectation of inflation even it is above the assumption of inflation on state budget at 3.1%. The government wasall out onmaintaininginflation in order to secure its position in 2019election. As the election is over, based on budget draft 2020, subsidy spending will be reduced to Rp199.7 tn.All in all, price changes remained stable in 2019, though it almost hit 3.5% on Aug-19, we expect YE 2019inflation at 3.3% YoY.

- Lower global oil price, lower subsidy on energy

After the reduced subsidy to Rp137.5 mn in 2019, the impact will be upon main people’s consumption. The price cut on subsidized fuel, Solar,by Rp1,000 is due to loweroil priceas we expect it will decrease to USD 60/barrel(Brent crude price) in 2020. Thus, current Solarprice ofRp 5,150/liter could rise to about Rp6,150/liter.Yet, the decrease on oil price may influence the decrease of other fuel price, like Pertalite (1.9%) and Pertamax (3.4%).

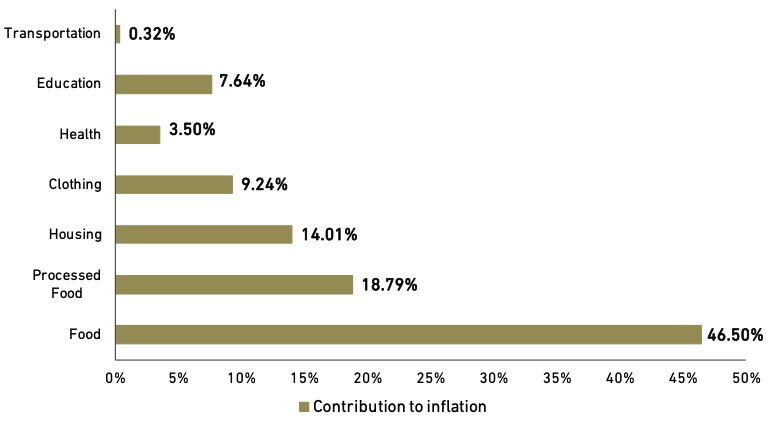

- Food still the main contributor of inflation

In Exhibit 8 we have summarized the contribution of the main component influencing inflation. Food is still the primary contribution of inflation, followed by the processed food. Due to the prolonged drought, Indonesia will face some delayed harvest season from the end of 2019 and 2020. Even in Oct-19 the season would be back to rain season, the government needs to put more attention on this changing. This climate irregularity and the subsidy cuts make us expect the inflation and core inflation to increase slightly at 3.5% and 2.9% YoY respectively in 2020 in line with the expected lower BI-7DRRR.

Exhibit 7: YoY Inflation and Policy Rate

Source: CEIC, BI, Ciptadana Estimation

Exhibit 8: Inflation Components Contributions

Source: BPS

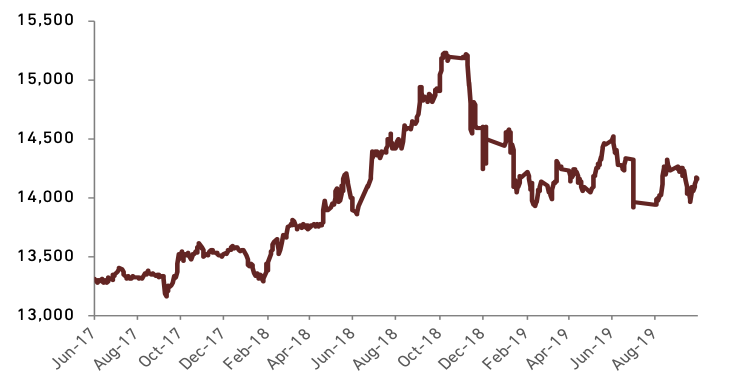

Pressured, but rupiah is getting stronger

Combination of global pressure and widening CAD led to pressure on rupiah, but somehow it appreciated slightly by 1.34% YTD to about Rp14,197/USD in Oct-19. In response, BI-7DRRR cut disincentives people to save rupiah on the bank or in other word money supply will increase; makes it loses its value. However, the decrease of FFR may create USD less attractive so IDR will be more attractive to hold even the impact is not that much since both rates fell off as well. Exhibit 9 shows how current account balance affects rupiah depreciation among years. By letting the CAD widening, it can reduce Indonesia foreign reserves. In 2Q19, Indonesia recorded USD8.44 mn of CAD which equals to 3.04% of GDP. Although in 1H19 Indonesia posted surplus on its balance of payment (BoP) by USD443 mn, we see that Indonesia will face a pressure on the weakening trade balance amid the getting stronger rupiah.

- External factors play bigger role on rupiah

On the last days of President Joko Widodo’s first term presidency, Indonesia was hit by massive demonstration erupted in response to a proposed criminal-code overhaul and other issues. Besides, Bank Indonesia has cut BI-7DRRR by 75bps so far to 5.25% as of Sep-19to keep up with the FFR cut. The unconducive moment and the rate cut may weaken rupiah since the riot may shape people’s disbelief to government and trigger the capital outflow.

However, the global economic downturn makes relatively more stable country like Indonesia to be more attractive for people to park their money. Especially, in 2020, the government has planned to attract investors more. Some powerful policies are super deduction tax and the on-the-making Omnibus Law which will regulate several types of taxes under one law. To support, the government will revise 72 Laws which hindered the investment to come.

- Stronger rupiah amid uncertainty

Above all, many believe that rupiah is mainly affected by external conditions that happen such as the trade war and FFR cut, not to mention that Trump impeachment issue may bring positive condition. Exhibit 10, shows that change in FFR may affect rupiah. Since we predict there will be another Fed rate cut until YE 2019 to 1.5% - 1.75%, we estimated that until the YE-2019, rupiah will stand at Rp14,190 with the average at Rp14,260 against dollar for full-year.

Exhibit 9: Exchange Rate (IDR to USD) and Current Account Balance

Source: Bloomberg

Exhibit 10: Rupiah and FFR Hike Expectation Shift

Source: Bloomberg

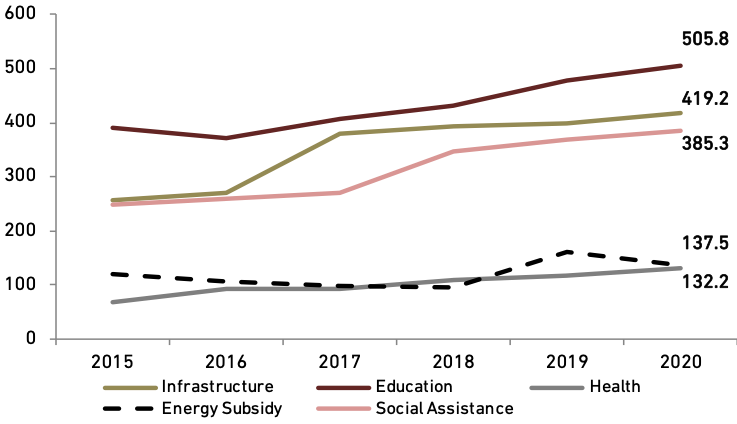

Government budget for development

Human capital development is fiscal mantra in carrying on into 2020. The draft of government budget for 2020 is focused on five aspects: human resources development, infrastructure acceleration, social protection programs, regional autonomy and anticipation of global uncertainties.

- Everything increased except energy subsidy

Government expenditure is set to increase by 7.9% from state budget 2019 outlook to Rp2,528 tn, still on prioritizing education sector. For education, the government allocated Rp505.8 tn with new allocation fund for college student assistance program. For infrastructure, the government allocated Rp419.2 tn especially to boost the connectivity as the government has focused on 4 super priority tourism destinations, they are: Toba Lake, Mandalika, Labuan Bajo and Borobudur. Social assistance spending was allocated to Rp385.3 tn which will be used to sustain the Indonesian conditional cash transfer program (PKH), non-cash food assistance (BNPT), and other assistances. On energy subsidy, the government cut the allocation by 24% to Rp137.5 tn. The cut seemed interesting because it was done right after the election year which from 2018 to 2019, there were 69% of increase of energy subsidy to Rp160 tn. There is an increase on the allocation for health to Rp132.2 tn. The government still finds a way to increase the fund by looking for new source of tax related to negative externalities.

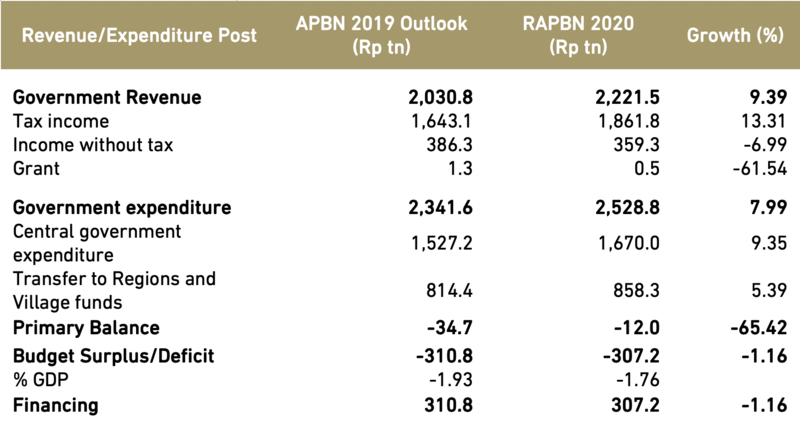

- Digging up potential in increasing revenue

Tax revenue improve in 2019, as of August 2019, tax revenue reached Rp1,189.3 tn, reaching 54.9% of target. This figure is lower than August 2018 performance when tax revenue reached 56.1% of 2018 target. The target of tax revenue itself was set on Rp1,861.8 tn and Rp359.3 tn for nontax revenue target. We expect 2019 tax revenue can reach higher even amid the limit space to move. In 2020, the government can optimize the super deduction tax program targeting the labor-intensive industries and R&D investments to accelerate economic growth. Alongside with the tax holiday, these measures will be challenging as the government faces slow growth in tax collection. Government deficit should be around 1.8% of GDP in 2019 and any potential shortfall of government revenue should be managed by reducing energy subsidy and being more selective on allocate money on less-prioritized project.

Exhibit 11: Government Expenditure Budget by Sectors

Source: MoF

Exhibit 12: Government Budget for 2019 and 2020

Source: MoF

Room for consumption and investment to grow

Consumption still became the main driver of growth as it grew 5.10% YoY in 1H19 with share to GDP by 54.3% This is followed by investment (GFCF) which grew 5.02% YoY in 1H19 and share to GDP of 32.3%. Consumption also denoted gradual recovery in 1H19 with 5.10% YoY growth after posting 5.05% growth on 1H18 and even below 5.0% growth in 2017. However, since the effect of election on consumption is over in 2H19 and amid the current weakening trade performance, we expect 2019 GDP growth to reach 5.01%.

- Positive sentiment to investment

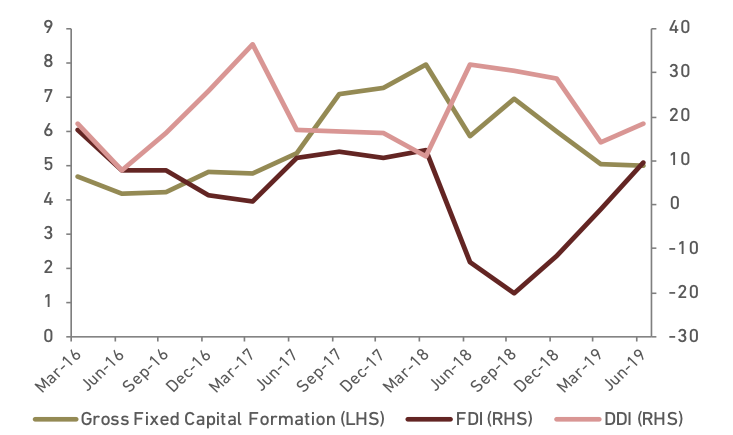

During 1Q18 to 3Q18 period, investment experienced significant plunge by 24.37% since in 2018 the Fed increased its rate by 100bps. However, the story should be different in 2019 as i) rupiah showed appreciation by 1.34% YtD until Oct-19, ii) Fed rate cut series and iii) the election result announcement was on May-19. Speaking of which, on 2014 election, the FDI rebounded after the announcement and we predicted the same trend will happen after the 2019 election year as well. The elected president seems to have clear stance in improving investment climate and this brings positive sentiment to market. It was proved by the increase of FDI growth by 9.61% or as much as Rp104.9 tn in 2Q19, preceded by negative growth series over year. The capital inflow was lured by the Fed rate cut and the global uncertainty. On exhibit 13, we see that domestic direct investment might help investment growth to increase when FDI growth was on negative territory.

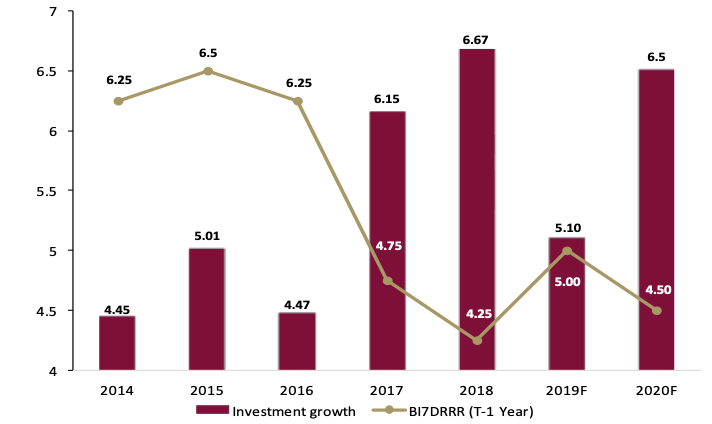

The lower BI-7DRRR decreases the cost of business financing. The lower credit rate usually needs 6-12 months (which means the mid of 2020 in current case) to feel impact from lower policy rate. In 2020, we predict the BI-7DRRR will go lower by 50bps to 4.50% to cope up with Fed rate cut and in order to boost the consumption and business expansion. However, we see there will be a room for investment in 2020 to grow supported by the lower policy rate due to the Fed rate cut that we expect will be cut again by 25 bps to 1.5% - 1.75% in 2020. Historically, investment growth experienced slow down due to higher rate in 2014 to 2016 while rate cut in 2016 gave significant boost to 2017 investment growth (see Exhibit 14). Based on our view above, we predict investment growth in 2020 to be higher at 6.1% YoY from 5.1% in 2019.

Exhibit 13: Gross Fixed Capital Formation and FDI Correlation

Source: BKPM

Exhibit 14: Policy Rate and Investment Growth in GDP

Source: Bank Indonesia, Bloomberg

- Challenges on consumption

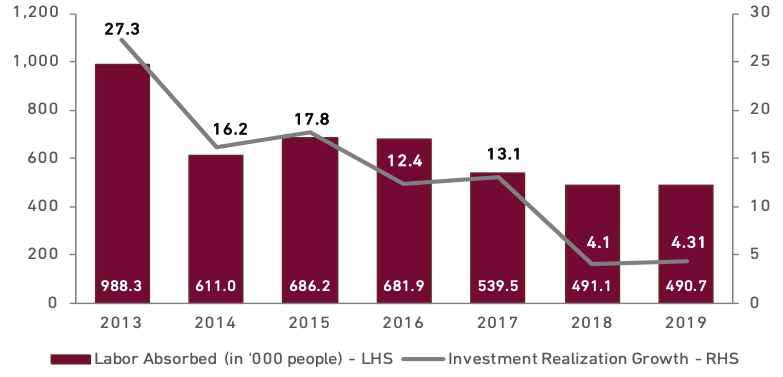

1H19 became the major sign of strengthened consumption growth as its growth reached 5.10% YoY after experiencing 5.05% growth in 1H18 and below than 5% in 1H17. However, we do not think the higher purchasing power came from “organic growth” or better labor profile. According to investment board, labor absorption from investment in 1H19 was not that much compared to 1H18 from Exhibit 15.Although it is notreflected in higher unemployment rate, lower absorption reduce the chance to get full time job. We view higher government social spending, election year and higher salary (+5%) for civil servants impact that played a significant role in raising consumption growth in 1H19.Entering 2020, consumption growth will still depend on government spending although there is a chance for investment to grow at 6.1% YoY so it may help labor absorption.

Government higher spending on social assistance by 4.4% YoY in 2020 will enable consumption to remain robust. However 2020 will be very challenging for expecting consumption to grow a strong as in 2019 due to the discontinuance of electricity subsidy on 900 VA consumers for about 27 mn households. In addition, there will be an increase on cigarette tax by 23% and raise of its minimum price by an average of 35% in 2020. The raise on excise tax may generate Rp172 tn of contribution to tax revenue in 2020 as well. This may bring a shift of consumption pattern among 57 mn smokers approximately in Indonesia. But, we believe it is insufficient to drastically alter the behavior. Given those conditions, we expect that consumption to face a slight contraction in 2020. We expect 5.0% consumption growth in 2019 and a slight decrease to 4.9% in 2020.

Exhibit 15: Investment Realization Growth and Labor Absorbed

Source: BKPM

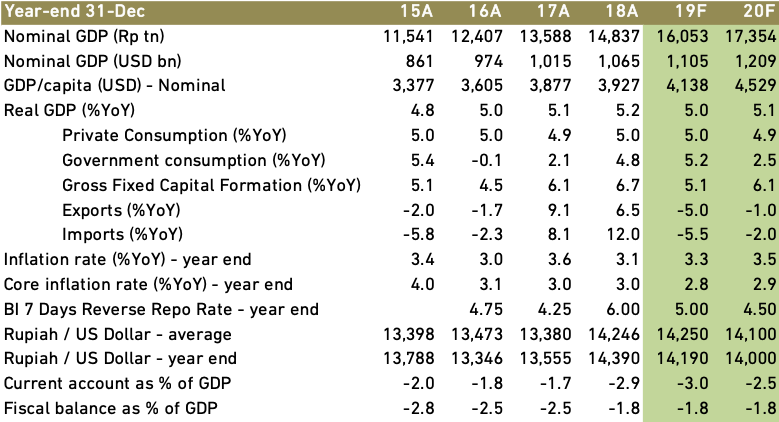

Exhibit 16: Indonesia’s Macroeconomic Projection

Source: BI, MoF, BPS, Ciptadana Estimates