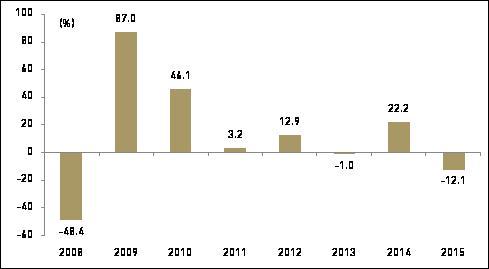

Review of 2015: Second worst yearly performance since 2008

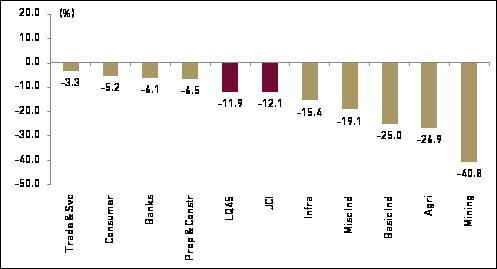

In 2015, the Indonesian equity market closed at 4,593, which fell short of our target by 6%, and ended 12% lower compared to 2014. This marked the second worst negative yearly return since 2008 and was also one of the worst performing regional bourses in US dollar terms (-21%) as Rupiah’s depreciation (-10%) underwhelmed performance. All sector indices posted negative return in 2015 with among major sectors that outperformed the market were trade & service which was down by only 3.3%. On the other hand, mining (-41%) and agriculture (-27%) were the most underperforming sectors on sharp decline in commodity prices.

JCI yearly performance

Source: Bloomberg

JCI and sector indices performances

Source: Bloomberg

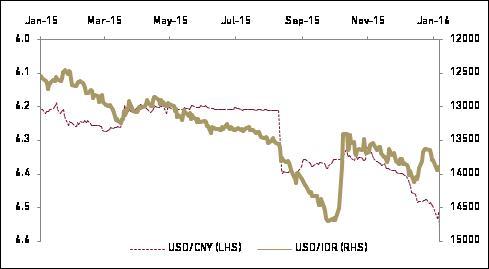

Overhang on US Fed removed but China’s factor to haunt

The Fed’s decision to hike its key interest rate from a range of 0% to 0.25% to a range of 0.25% to 0.5% in Dec-15 was in line with our expectation. This should partially end uncertainly that clouded equity market previously. Our economist expect subsequent hike of 50bps at end 2016, which we believe will be welcomed by market too. However, we continue to see risk from China’s economic struggles that have been a key factor in the recent market volatility. We believe no one can predict if it would be a soft or a hard landing for the Chinese economy. But one thing for sure is that the world financial markets cannot afford sudden devaluation of the Chinese currency, which was seen in 2015. China is making structural changes by focusing on being a domestic lead economy rather than export driven. Until then it would mean that China will keep on depreciating its currency to keep its exports competitive. Indonesia is susceptible to a China growth slowdown and potential Yuan devaluation. However, we believe that these risks are better priced now as Rupiah has already weakened sharply in 2015 (reached lowest level of 17%). Our economist expect Rupiah to further weaken by 5% to 14,500/USD at end of 2016, mostly on further Fed rate hike, which we view quite more favorable than in 2015.

Strong correlation (0.74) between CNY and IDR

Source: Bloomberg

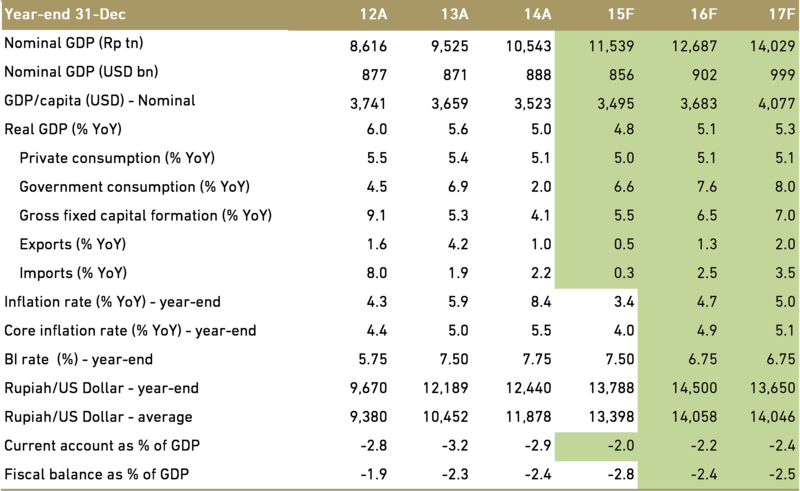

Economic optimism to underpin equity market

We believe investor interest continues to remain strong as favorable macro cues such as higher GDP growth, low inflation, potential declining interest rates, higher infra spending are likely to drive improvement in corporate performance. Our economist expects GDP growth to pick up from 4.8% in 2015 to 5.1% in 2016, due largely to higher government spending (+7.6%) and investment (+6.5%). Inflation should moderately increase from 3.4% to 4.7%. The contract infrastructure project signing of Rp25 tn YTD already represented 6% of ministry of public works budget spending, very significant improvement as in last year the achievement was only reached in June. Furthermore, the current account deficit (CAD) is likely to remain at manageable levels, despite widening from 2.0% to 2.2%. With inflation likely to fall back within Bank Indonesia’s target range of 3%-5% throughout 2016 and Fed would not aggressively raise rate, we believe it opens up room for BI to cut rate in 2Q16 by 75bps to 6.75% which should be supportive of equities. Meanwhile, we see events like potential cabinet reshuffle and the pass of tax amnesty bill as near term catalysts. The potential entry of National Mandate Party (PAN) will inevitably help the government secure more support from the House and will help to assist Jokowi’s policies through the legislative branch of the government. PAN will bring “government coalition” seat in legislative branch to 256 seats vs. number of seat held by the opposition Red-and-White Coalition (KMP) of 243 seats. Meanwhile, the government estimates tax amnesty will lure back money stashed overseas to net an extra USD4.4 bn of revenue this year.

Our key macro assumptions

Source: Bloomberg and Ciptadana estimates

Attractive backdrop for Indonesian equity

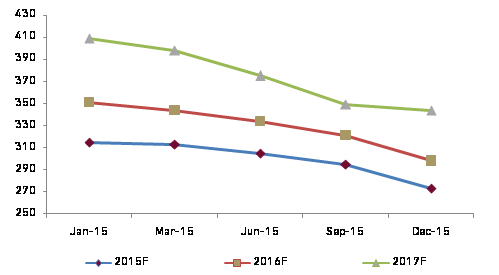

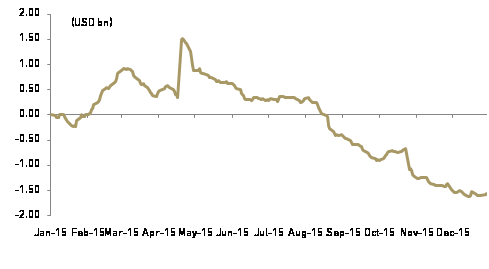

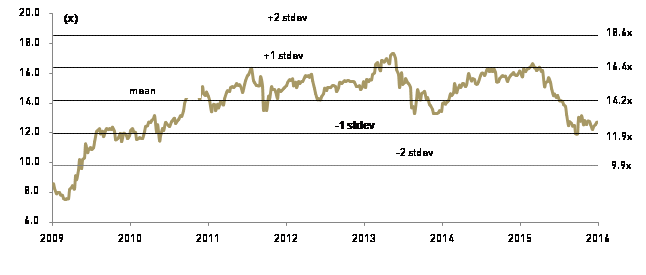

After a disappointing 2015, investors will be hoping for an earnings recovery although we think strong signs are likely in 2H16 post cut in BI rate. Consensus market EPS forecasts continue to trend down, especially after a lackluster 3Q15 reporting season. Thus we believe less downside risks to consensus market EPS forecast going forward. We forecast 2016-2017 market EPS growth of11%-12%, based on 72 stocks under our coverage that make up 71% of JCI market capitalization. Valuation is now at 12.8x forward PER (excluding HMSP) modestly below the 5-year mean of 14.2x. Furthermore, we see limited downside risks from foreign selloff after net foreign outflows have aggregated to around Rp21.7 tn (USD1.58 bn) over the last year. Therefore, we maintain our overweight stance on JCI and end-2016 JCI target of 5,700, which implies 13.9x forward PER.

Market EPS consensus

Source: Bloomberg

Accumulated foreign investor net buy (sell) in 2015

Source: Bloomberg

JCI forward PER

Source: Bloomberg