Construction Overweight

Sector Outlook

- A slow growth in infra spending

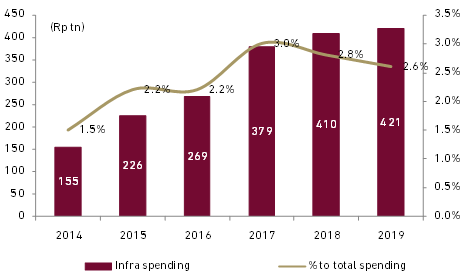

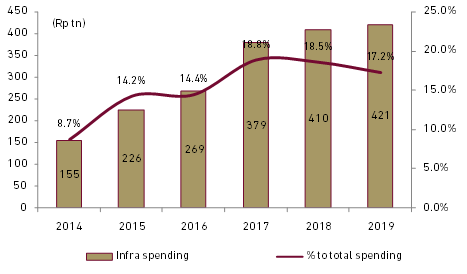

In the 2019 state-budged, the government raises infrastructure budget by only 2% YoY to Rp420.5 tn vs 27% CAGR in 2014-2018. Despite the 2019 infrastructure spending only inching up, it actually remains high in term of 1) as percentage to total government spending of 17.2% vs 2015-18 average of 14.9% and 2) as percentage to GDP of 2.6% vs 2015-18 average of 2.3%. We see government more focus toward social spending ahead of president election while planning to limit imported products related to infrastructure projects. Indonesia has been prone to global economic shocks as the country has been persistently running budget and current-account deficits. The government plans to build 667 km of new roads, 905 km of toll roads, 48 dams, and irrigation system to cover 162,000 hectares of rice paddy fields. We are not too concerned about slowing growth in infrastructure spending as government (budget-funded) project accounted for on average 19% of contractor’s new contract as of 8M18. Meanwhile contract from SOEs and private projects represented 49% and 32% of total contract, respectively. Government import restrictions plan might have impact contractors EPC project which comprises between 12-16% of total contract as of 1H18.

Exhibit 112: Infra spending as % of GDP

Source: Ministry of Finance and Ciptadana Sekuritas

Exhibit 113: Infra spending as % of total government spending

Source: Ministry of Finance and CiptadanaSekuritas

- New contracts decelerates but order book remains solid

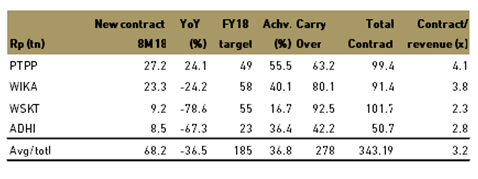

Most of SOEs contractors saw declining new contract growth this year which we believe attributable to 1) high base effect from 2015-17 large scale projects such as greater Jakarta and Palembang LRT, trans-java toll roads and PLN transmission projects, etc. 2) Managements prefer to slowdown projects completion following several accidents in 2017 and 2018. 3) Slow progress in contract payment that might have affected contractors cash flow and 4) funding constraint on higher debt and expectation of rising cost of fund on higher-than-expected interest rate hike this year.

The aggregate new contracts of SOE contractors under our coverage was down 36.5% YoY in 8M18 with WSKT reporting the largest decline of 78.6% YoY to Rp9.2 tn, while PTPP was the only company booking positive growth of 24.1% YoY to Rp27.2 tn. WIKA and ADHI also registered negative growth in new contracts of 24.2% and 67.3% YoY. Comparing to their respective full-year target, PTPP was also the best performer achieving 55.5% of 2018 target, followed by WIKA of 40.1% and ADHI of 36.4% while WSKT only achieved 16.7% of target. WSKT just recently cut its target from Rp70 tn previously to Rp54-55 tn. On average, the aggregate 8M18 new contracts only accounted for 36.8% of full-year target, or lower than historical average of 42.6%.

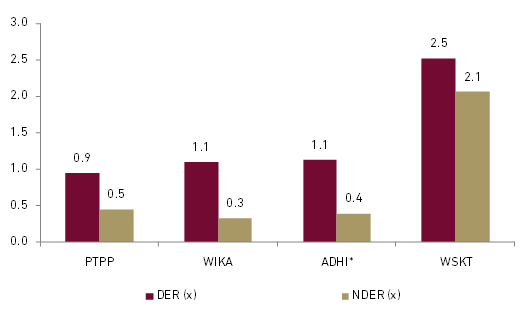

We still view that slower growth in new contract will not immediately hurt earnings outlook given as most of contractors are sitting on higher oderbook which is equivalent to 3.2x annual review. New contracts could improve in 2H18 as the acceleration in infrastructure project will be faster in 2H due to the backend loading of infra-spending. Moreover, contractors under our coverage still book higher earnings growth in 2Q18 by 68% on average. Most contractors, except WKST, have also relatively good balance sheets to support new contracts growth and investment. The companies diversifying business to infrastructure such as power plant, toll road, TOD or townhouse to enlarge orderbook . As at end of June 2018, PTPP has the least leverage balance-sheet with DER of 0.9x (NDER: 0.5x) followed by WIKA with DER 1.1x and NDER of 0.3x. WSKT has more leverage balance sheet with DER of 2.5x (NDER of 2.1x). The leverage are so far below their debt covenant level of around 3.0-3.5x

Exhibit 114: SOE contractors contracts

Source: Companies and Ciptadana Sekuritas

Exhibit 115: SOE contractors DER and NDER

Source: Companies and Ciptadana Sekuritas. * ADHI as of Mar-18

- The sector saw a heavy correction , trading at depressed valuations

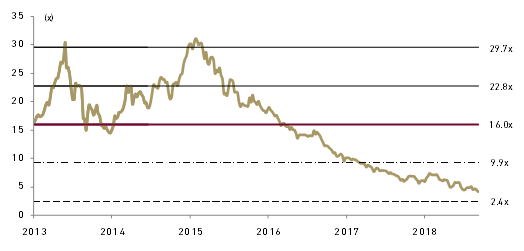

The construction sector plunged about 28% Ytd, underperforming the JCI significantly by 36%. The investor’s concern on slowing contract growth, cash flow and balance sheet has taken a toll on the construction sector this year. The construction stocks are down between 37% and 55%from their respective 52-week highs, which include names such WSKT (-46%), PTPP (-55%), WIKA (-37%) and ADHI (-47%) . On Ytd basis, the construction stocks are down between 10-43%,The sector valuation has seen severe de-rating to only 4.1xforward PER or only slightly above -2stdev historical mean of 16.0x. It is also far below the sector historical mean from the pre-Jokowi era 20.1x.

Exhibit 116: Construction sector valuation (forward PER)

Source: Bloomberg and CiptadanaSekuritas

We do not expect to see the glamour part of the construction sector where it has been trading at significant premium to market valuation in the past, given that the sector faces decelerating new contract growth. However, we still expect a rebound in construction sector next year on sector rotation and historically the construction sector saw re-rating during election year. Moreover, we believe Indonesia infra still has the most promising long-term outlook given its need for massive upgrade. We have buy rating for all contractors under our coverage given their attractive valuation and we believe current depressed valuation creates buying opportunity. We select PTPP top pick due to 1) positive new contract growth, 2) double digit earnings growth in 2019F, 3) stronger balance sheet will help it to tackle future funding problems , and 4) more conservative approach to win the contract reflected in its diversified contracts and 5) the most underperforming contractor which we believe due mostly to higher foreign ownership exposure. The table below shows our pecking order in construction sector as well as their rating and valuation.

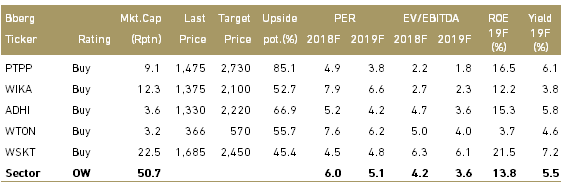

Exhibit 117: Construction stocks rating and valuation