Coal

Overweight

Sector Outlook

- 2017: Supply capped by weather, hoist prices

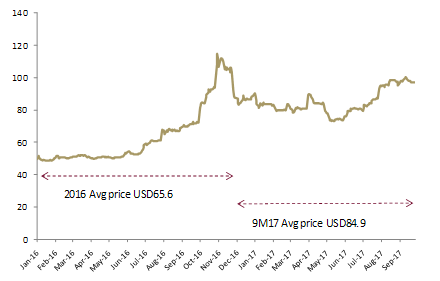

The Newcastle coal price was gradually down and bottomed at USD73.3/ton in mid-May’17. The Chinese Government’s decision to loosen the 276 working days ban has put a pressure on coal price. However, price started to increase afterward, as heat wave moved across China causing higher power demand for air conditioning, while raging floods from torrential rain, causing under utilization of hydro power. In general, production increased but not at fast speed, as mine accidents delayed China’s resuming production. China imported more high calorific coal, while demand from Taiwan, South Korea, and South East Asia for low-grade coal improved due to electricity demand. As a result, average coal price in 2017 is expected to hover at USD85/ton, higher than our previous estimation of USD75/ton.

China is expected to launch new regulation related to coal inventory in 4Q17. This will trigger demand, mostly until 1Q18, since average coal inventory at IPPs stands far below the required standard stated in the draft (14 days of coal inv. vs the standard of 20 to 25 days). However, in general, we view China’s demand for coal will only grow by 2.3% (vs 3.4% average in 2007 – 2012, and 2.6% 2017’s growth forecast), as China continues to reject several proposals for new coal-based power plants. Domestic demand will continue to grow along with the completed construction of new power plants, but not as high as expected, as PLN recalculates the upcoming domestic needs.

- Supply to decline due to capacity reduction

China is likely to continue to curb supply by closing illegal and irresponsible miners, which in our calculation will reduce by 300 mn tons of production in 2018,as it aims to manage domestic coal prices better and reduce air pollution. Given the above demand and supply forecast, we expect China coal market to continue deficit, but with lower amount of 158 mn tons (vs 201 mn tons in 2016). This will intensify competition from Indonesia and Australia. In India, domestic productions will once again outpaced demand. In Australia, production is forecasted to increase marginally, to 251 mn tons. All in all, as we still see deficit in global coal industry, we expect coal price to stay at healthy level of USD85/ton in 2018.

- US coal industry remains stagnant

Although US Government plans to reward coal-fired power plants that keep stockpiles for at least 90 days, signaling intention to reawake the industry, but the core problem, which are flattened U.S. electricity demand and stolen market share from natural gas, wind and solar power, should be addressed first. To that end, we doubt the reward is enough to bring back US coal.

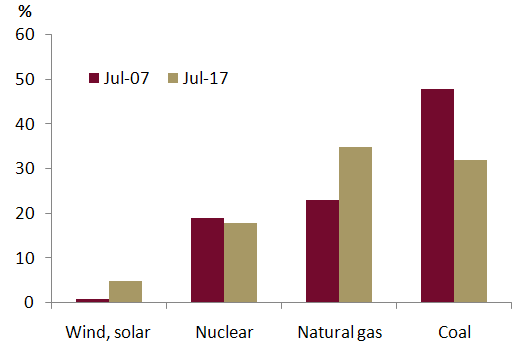

Exhibit 55: Contribution to US energy

Source: US Energy Information Administration

Exhibit 56: Newcastle coal price for thermal coal (USD/ton)

Source: Bloomberg

- Loan for coal miners remain limited

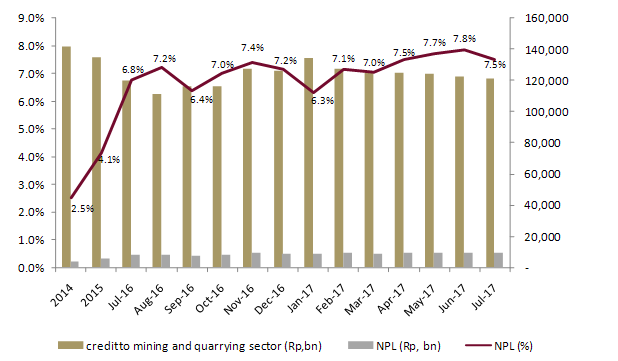

We believe that banks will continue to put brakes on loan to mining industry (mostly coal companies), as they tend to lower the bad debt first before pouring funds to the industry. Banks is also reluctance, since other sectors, i.e. construction, looks more promising. Stable high coal price may help miners to reduce bad debt, but we believe it will take more than one year to bring the NPL down to around 3%. Thus, coal miners will continue to rely on internal cash or other sources of financing to fund their capex plan.

Exhibit 57: NPL and loan to mining and quarrying industry

Source: Bank Indonesia

- ASP to benchmark price ratio to narrow

Given its low calorific value, Indonesian coal miners’ ASP was relatively at a discount compare to the benchmark (Newcastle). Such discount was widened in 2016 as most miners sold its coal at forward fixed price, causing average sales price to lag the rise of benchmark prices (please see appendix). In 2018, such gap should be narrowed, with Arutmin owns the largest opportunity for improvement.

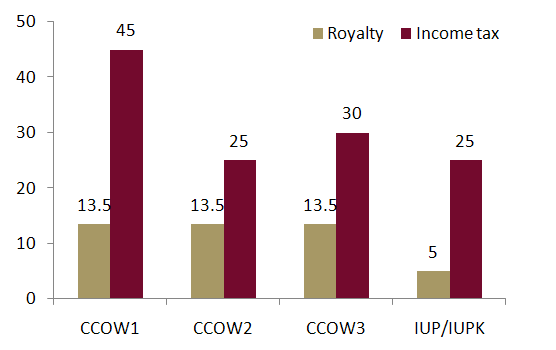

- To benefit from government’s plans to lower royalty and tax

Most of miners’ first generation coal contract of work (CCOW1) would expire over the next few years. And according to 2009 Mining Law, it should be converted to IUPK at maturity, the latest. Prevailing royalty and income tax rate for CCOW1 is 13.5% and 45%, respectively, and expected to reduce to 5% and 25% respectively, if government’s new regulation is enacted. We view that ADRO will be benefitted the most from the upcoming regulation, not only because they owns CCOW1 but also due to long reserves life.

- More M&A transactions and moving to downstream sector

M&A transactions among Indonesian coal miners is expected to increase, as miners try to capitalize on the price recovery, increase their reserves, and avoid increasing costs of energy sources (as PLN is now trying to do). However, we see that valuations for coal miners as well as financing for M&A as the hurdles for such process. More miners also try to enter downstream sector, particularly by building power plant, to secure stable revenue stream ahead.

Exhibit 58: Royalty and income tax rate (%)

Source: Ministry of Finance

- Our stocks pick and rating

We select PTBA as our top pick in coal sector due to 1) its higher profitability margin and ROE, 2) no more negative sentiment from domestic coal price cap, 3) in terms of valuation, PTBA is relatively undemanding with 2018F PER of 6.0x, below average peers of 7.0x.

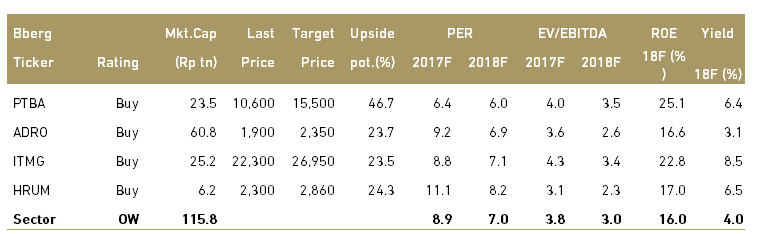

Exhibit 59: Coal stocks rating and valuation