Economic Outlook

Global economic outlook:

Prospects for 2023 and a path to recovery in 2024

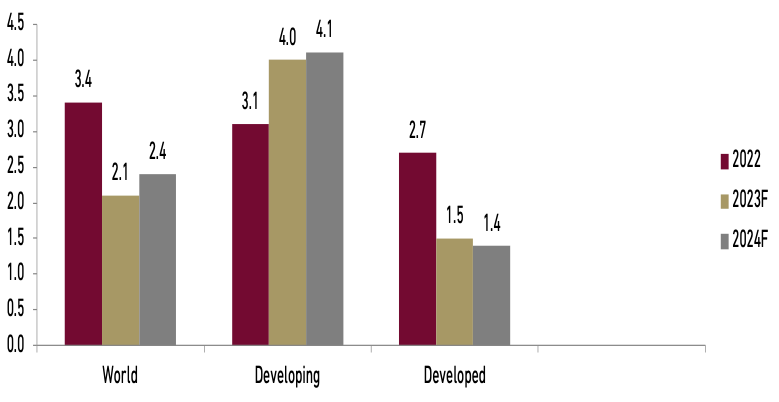

Global economic growth, which is on a slowing trend in 2023, is expected to improve slightly in 2024. According to the World Bank, global economic growth is expected to slow from 3.4% YoY in 2022 to 2.1% YoY in 2023 and then recover to 2.4% YoY in 2024. In parallel with this economic growth trajectory, global trade volume, which is expected to grow by 5.2% yoy in 2022, is projected to slow to 2.0% YoY in 2023, but rebound to 3.7% YoY in 2024. Developing countries are expected to play a key role in driving the global economic recovery in 2024 amid sluggish economic growth in developed countries (see Charts 1 & 2).

Exhibit 1: Developing and developed economic growth forecast

Source: World Bank

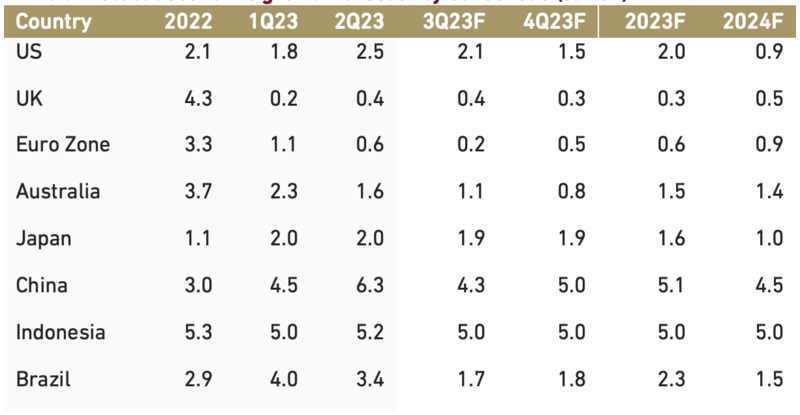

Exhibit 2: Global economic growth forecast by consensus (% YoY)

Source: Bloomberg

- Global inflation trends: 2023 challenges and hope for 2024

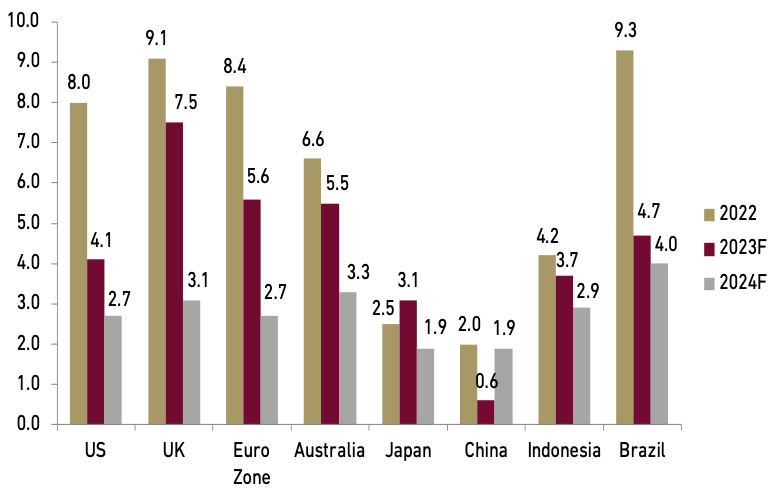

The World Bank expects the global inflation to reach 6.8% YoY in 2023 but is expected to ease approximately at 5.2% YoY in 2024. The trend of moderating inflation and a reduction in the intensity of monetary tightening policies will create space for global recovery in 2024. Although global inflationary pressures have subsided since 2023, there remains a potential for persistently high inflation that could exceed the medium-term targets in several developed countries. Based on consensus, Both inflation rate in US and Euro zone are predicted to be 2.7% YoY in 2024, surpassing their inflation target at 2.0% YoY (see exhibit 3).

Exhibit 3: Inflation growth forecast by consensus (% YoY)

Source: Bloomberg

- Monetary and fiscal policy in 2024: Divergent paths amidst easing inflation

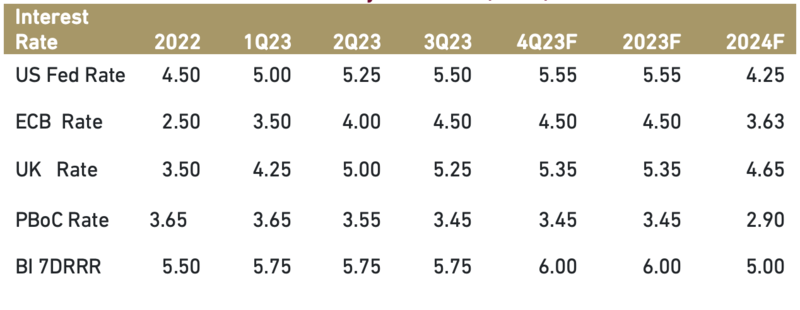

As global inflationary pressures continue to ease, the monetary tightening in 2024 is expected to diminish, and several countries are likely to adopt more accommodating monetary policies (see exhibit 4). From the fiscal side, we expect that developing countries will implement accommodative fiscal policies to encourage economic growth in 2024. On the other hand, fiscal support in the European countries tends to be more limited due to persistently inflationary pressures.

Exhibit 4: Central bank rates forecast by consensus (%YoY)

Source: Bloomberg

- China's economic challenges and strategies for 2024: Navigating a slower growth path

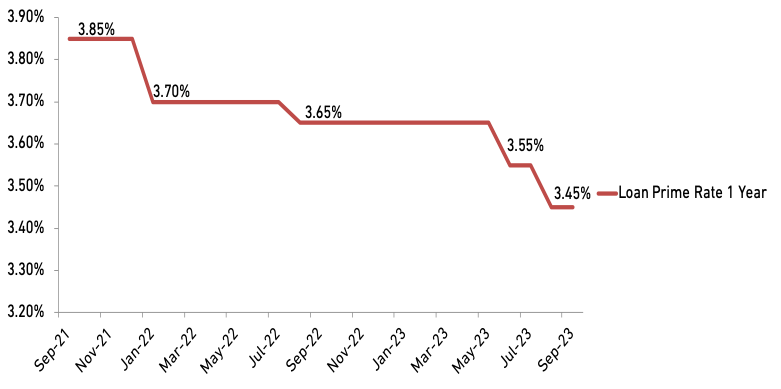

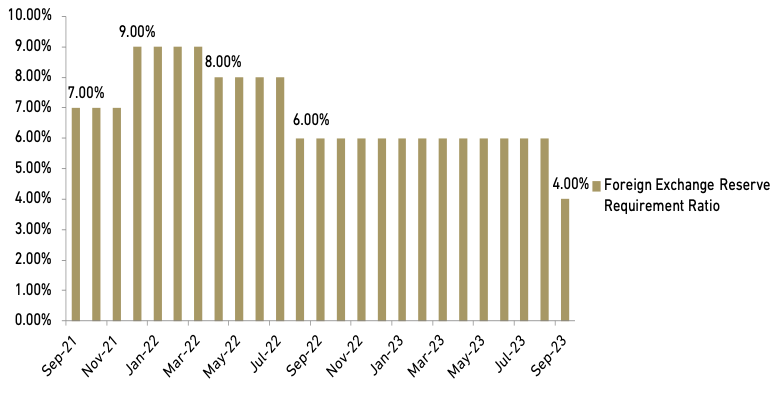

China's economic growth is expected to decelerate in 2024, following a rebound from the pandemic in 2023. Any reopening that falls short of expectations is expected to impede recovery in 2023 and hinder the pace of future economic revival. According to projections from the International Monetary Fund (IMF), China's economy is expected to grow by 5.2% YoY in 2023 but is predicted to slow down to a growth rate of only 4.5% YoY in 2024. Similarly, the World Bank forecasts China's economic growth to decrease to 4.6% YoY in 2024. Factors such as weak external demand, high debt levels weighing on the property sector, and reduced stimulus for infrastructure have the potential to constrain investment growth. Nevertheless, China's economy continues to receive support from the trade and services sectors, as well as robust consumption. We expect that China will implement accommodative fiscal and monetary policies in 2024, especially in the property sector to stimulate economic growth. Currently, China is providing significant stimulus by lowering the policy rate and reserve requirements (see exhibits 5 and 6).

Exhibit 5: China loan prime rate 1 year

Source: Bloomberg

Exhibit 6: China foreign exchange reserve requirement ratio

Source: Bloomberg

- Challenges and strategies for the us economy in 2024: Balancing monetary tightening, inflation, and fiscal policy

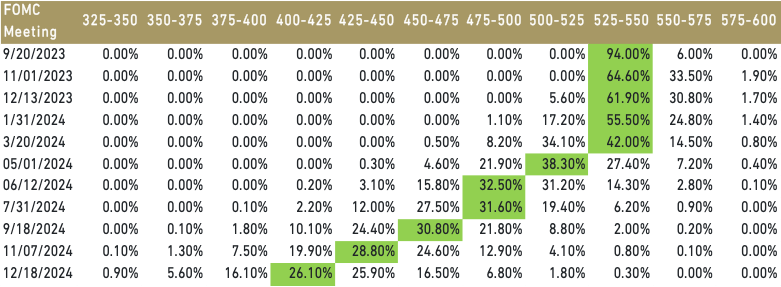

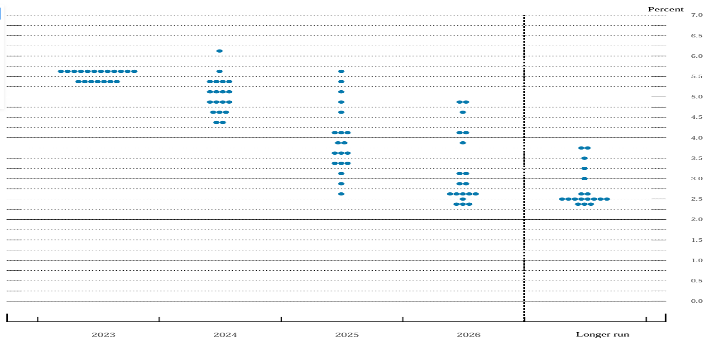

The impact of tight monetary conditions on the US economy is expected to persist into 2024. According to the IMF's predictions, US economic growth is projected to slow from 1.8% YoY in 2023 to just 1.0% YoY in 2024. Meanwhile, the World Bank estimates that US economic growth in 2024 will be even lower, at 0.8% YoY. The disruption to the US economic recovery can be attributed to the aggressive tightening of monetary policy since 2022 and the persistent issue of high inflation. With inflation rates remaining above the medium and long-term targets, interest rates are expected to remain high and pose a challenge to the expansion of economic activity in the US. Based on the market expectations captured by CME Fedwatch, it is indicated that the Fed Funds Rate (FFR) benchmark interest rate will remain steady at 5.50% by the end of 2023 and decrease to 4.25% by the end of 2024 (see exhibit 7), meanwhile Fed dot plot projects the FFR will increase by 25 bps to 5.75% in the end of 2023 and down turn to 4.75% by the end of 2024 (see exhibit 8). To mitigate the potential economic shock, the US government will provide accommodative fiscal policy. This includes incentives aimed at improving supply chains, supporting the green economy sector, and bolstering the healthcare sector under the framework of the Inflation Reduction Act (IRA). While these measures are beneficial for the US economy, they have a potential negative impact on investment flows in developing countries.

Exhibit 7: Fed meeting target rate probabilities

Source: CME Fedwatch

Exhibit 8: FOMC participants view on future monetary policy

Indonesia’s Economic growth outlook for 2024:

Optimism amid global rebound

We expect Indonesia's economic growth to accelerate to 5.2% YoY in 2024, up from our forecast of 5.0% YoY in 2023. According to our forecast, household consumption will be the main contributor to economic growth in 2H23, contributing 54% of GDP, supported by controlled inflation, enthusiasm in demand and election spending. We also expect household consumption to grow by 5.3% YoY in 2024. The second largest contributor to economic growth will be gross fixed capital formation (GFCF) or investment, accounting for 30% of GDP, supported by the downstream commodity policy, the infrastructure budget and the omnibus bill. We expect investment to grow 4.9% YoY in 2024. Both exports and imports are expected to grow by 7.5% YoY and 7.2% YoY, respectively, in 2024, in line with the global economic recovery and downstream policies. However, we expect the prices of key export commodities such as coal and CPO to continue to decline in 2024 compared to 2023, although they are expected to remain higher than pre-Covid pandemic levels. We expect government consumption to rise 5.3% YoY in 2024, slightly higher than the 5.2% YoY increase in government consumption expected in 2023. This increase will be driven by elections and infrastructure development.

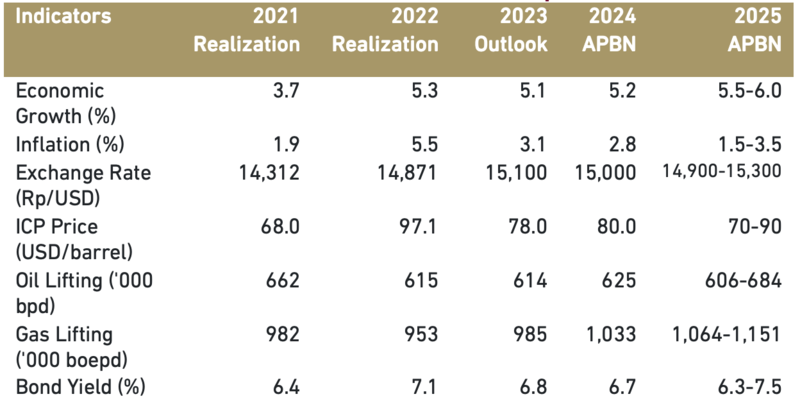

Meanwhile, Chart 9 shows the assumption for macroeconomic variables in the fiscal position (APBN).

Exhibit 9: Government’s macroeconomic variables assumptions

Source: Ministry of Finance

- Household consumption: Driving force of economic growth in 2024 amidst optimism and potential challenges

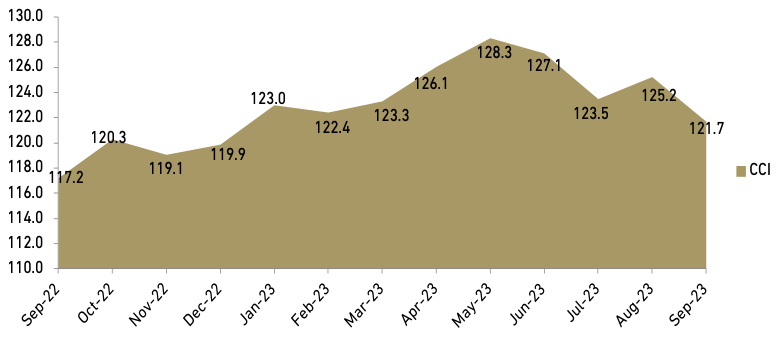

Our forecasts indicate that household consumption will be the main contributor to economic growth in 2024, accounting for 54% of GDP. This growth will be supported by factors such as controlled inflation, increased demand enthusiasm, and increased spending during the election campaign period. In addition, the proposed 8% salary increase for government employees and more national holidays would encourage individuals to increase their consumption. In addition, according to BI's consumer survey, the Consumer Expectation Index (CEI) stood at 131.3 in September, indicating optimistic consumer expectations for the next six months. In addition, the Consumer Confidence Index (CCI) remains in optimistic territory, although the latest reading declined (see Chart 10). As a result, we expect household consumption to grow 5.3% YoY in 2024, up from our forecast of 5.2% YoY in 2023. While the outlook for consumption remains strong, the expectation of a higher for longer Federal Funds Rate (FFR) stance and China's economic slowdown may remain as potential threats.

Exhibit 10: Indonesian Consumer Confidence Index (CCI)

Source: Bank Indonesia

- Investment prospects in 2024: Political stability and strategic initiatives

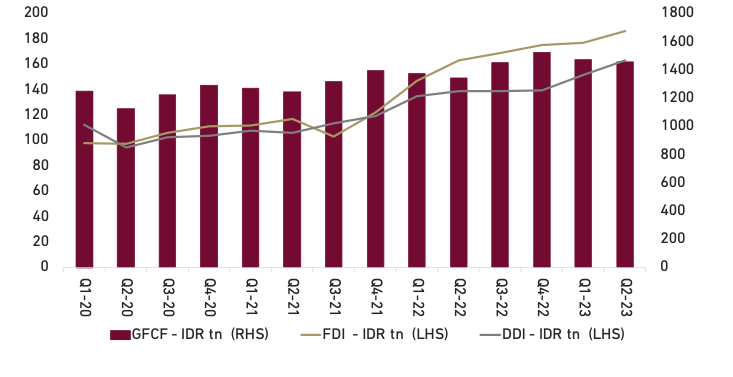

We observe that political stability is being maintained in the 2024 general election. It appears that all presidential candidates are committed to continuing the downstream project and relocating the new capital city to Ibu Kota Nusantara (IKN). The continuation of downstream projects will further enhance interest and attractiveness for investment in the country. There is a significant increase expected in the construction of smelter facilities for strategic minerals such as nickel, bauxite, and copper, aligning with the government's policy to promote expansion in these sectors. Investment in housing is also anticipated to rise as people's purchasing power increases. Bank Indonesia (BI) is expected to maintain loose macroprudential policies in the housing, downstream, agriculture, tourism, green funding, and MSME sectors. Additionally, the government is accelerating investment through state spending instruments by completing national strategic projects, priority infrastructure, and the IKN capital project. Our estimates suggest that Gross Fixed Capital Formation (GFCF) will grow by 4.9% YoY in 2024, surpassing the previous year's forecast of 4.2% YoY. Furthermore, both Foreign Direct Investment (FDI) and Domestic Direct Investment (DDI) show a positive trajectory (see exhibit 11). We believe that Indonesia is on track to achieve its investment target of Rp1,400 tn in 2023 and Rp1,650 tn in 2024.

Exhibit 11: GCFC, FDI, and DDI

Source: BPS and BKPM

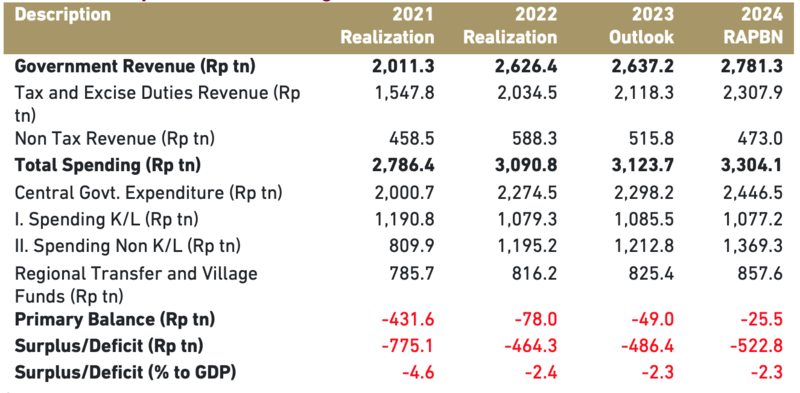

- Indonesia's fiscal outlook for 2024: Balancing revenue growth and expenditure priorities

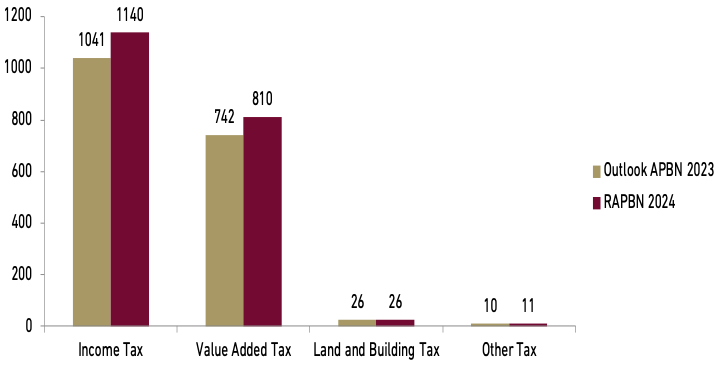

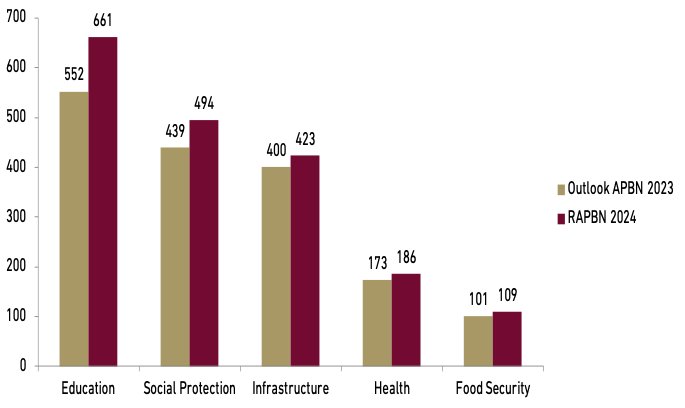

President Joko Widodo unveiled his final state budget on August 16, 2023, emphasizing the importance of maintaining a 'healthy' fiscal position in the upcoming year. In his speech, the projected state revenue is expected to increase by 5.5% YoY to Rp2,781.3 tn, while expenditures are expected to grow by 5.8% YoY to reach Rp3,304.1 tn in 2024. We expect that tax revenues will continue to rise in line with projected economic growth, despite challenges such as the risk of a global economic slowdown and commodity price volatility. Additionally, we project rapid growth in the digital economy, highlighting the need for the government to optimize taxes from this sector. Besides, income tax is expected to be primary government revenue followed by value added tax, and land and building tax, aligning with outlook APBN 2023 and RAPBN 2024 (see exhibit 12). Regarding government consumption, we believe that education, social protection, and infrastructure will be main focus on government spending, aligning with APBN 2023 and RAPBN 2024 (see exhibit 13). Overall, we project a 5.3% YoY increase in government consumption in 2024, slightly exceeding the 5.2% YoY government consumption expectations for 2023.

Exhibit 12: Government revenue by types (Rp tn)

Source: Ministry of Finance

Exhibit 13: Government spending by functions (Rp tn)

Source: Ministry of Finance

- Export prospects for 2024: commodity price challenges and growth opportunities

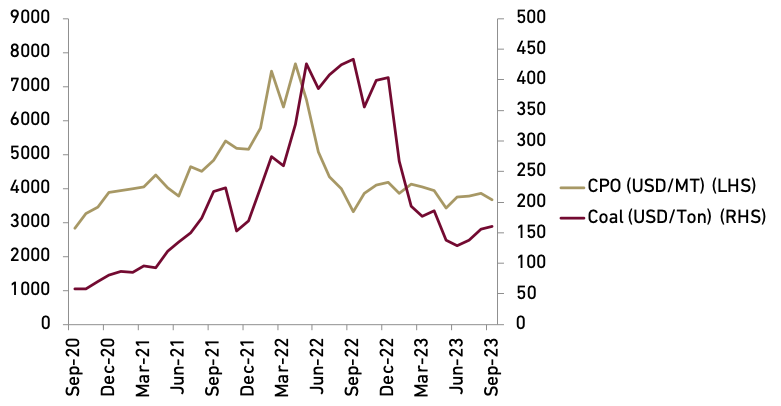

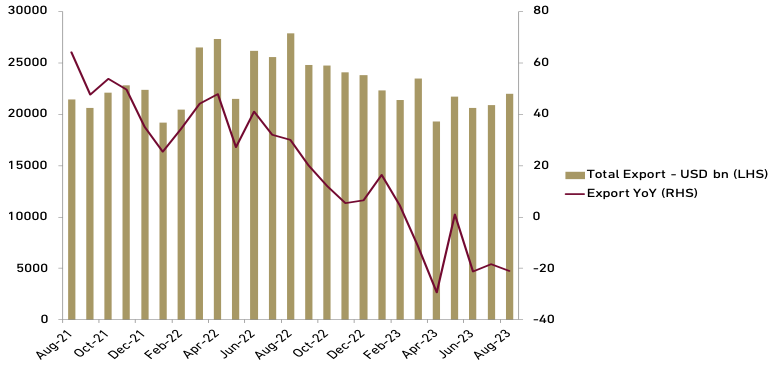

The expansion of natural resource downstreaming is set to play a pivotal role in driving export performance in 2024. Additionally, the progressive construction of nickel processing facilities which is scheduled to start operating in 2024 will have a positive impact to export growth. However, we anticipate that the prices of key export commodities like coal and CPO in 2024 will continue to decline compared to 2023, albeit remaining higher than pre-Covid pandemic levels. Several factors contribute to the depressed coal prices, including stock recovery in European countries, China, and India, expectations of reduced coal imports by India and China due to domestic production policies, increased global coal supplies from producers like Indonesia and Australia, and the anticipated decline in global coal demand due to energy transition initiatives. As for CPO prices, it is predicted to decline primarily due to the European Union Deforestation Regulation (EUDR). We believe that the EUDR policy could potentially disrupt Indonesia's plantation and forestry sector export performance. Therefore, the government should engage in diplomatic efforts to ensure that the EUDR does not become a non-tariff barrier for Indonesia's exports. Despite these challenges, we expect exports to grow by 7.5% YoY in 2024, showing resilience in line with the rebound in global economic growth for the 2024. On the other hand, we anticipate that total exports will decelerate to -0.12% YoY in 2023 due to moderating commodity prices and a global economic slowdown (see exhibit 14: CPO and coal prices as the main export commodities decrease). Meanwhile, exhibit 15 shows that total exports and export growth are diminishing.

Exhibit 14: CPO and coal price

Source: Bloomberg

Exhibit 15: Total export and export growth

Source: BPS

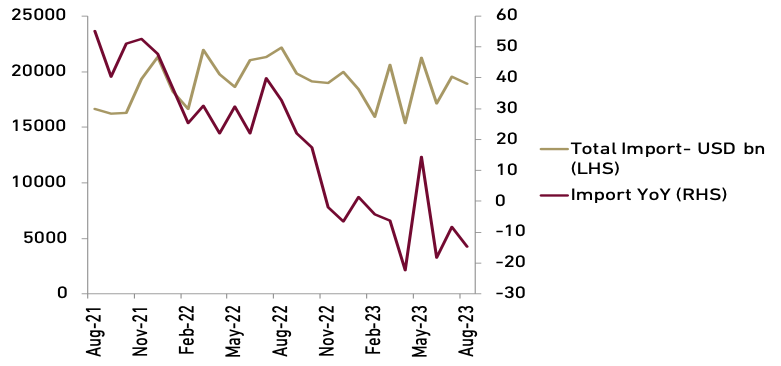

- Import growth trends in 2024: Boosted by investment and consumption optimism

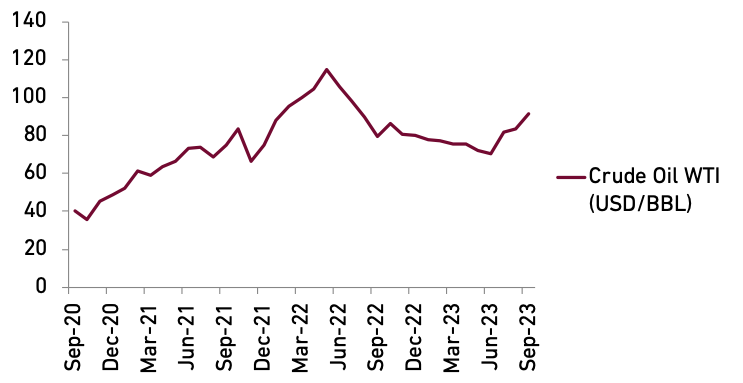

In 2024, imports of both capital and consumer goods are showing positive growth trends, indicating a favorable outlook for investment and consumption. The surge in capital goods imports can be attributed to robust foreign direct investment (FDI), particularly in machinery used in mining and manufacturing. Key drivers for this investment boost in 2024 include downstream commodity policies and an omnibus law. Moreover, the government has set an ambitious investment target of Rp1,650 tn in 2024, surpassing this year's target of Rp1,400 tn. On the other hand, the increase in consumer goods imports appears to be linked to higher household consumption, supported by accelerated GDP growth and controlled inflation rates. Several indicators, such as the Purchasing Manager Index (PMI) and Consumer Expectation Index (CEI), further bolster the import growth. PMI was recorded at 52.3 in September 2023, marking the 25th consecutive month of expansion. Meanwhile, CEI stood at 131.3 in September, signifying heightened consumer expectations for the next six months. We expect that both PMI and CEI will maintain their positive trends throughout 2024. From the perspective of key imported commodities, the price of crude oil is expected to rise in 2024 due to concerns about continued production cuts by Saudi Arabia and Russia. Crude oil price has increased by 15.36% YoY to USD 91.7/BBL (see exhibit 16). The government has revised its oil outlook, specifically the Indonesian Crude Price (ICP), from USD 78 per barrel in 2023 to USD 80 per barrel in 2024. Furthermore, we project that imports will decelerate by -0.45% YoY this year and rebound to 7.2% YoY in 2024. Look at exhibit 17 for the total import and import growth trend.

- Current account deficit widening due to primary income deficit

While the downstreaming of natural resources has the potential to increase exports relative to imports, resulting in a trade surplus, it also has the potential to increase the deficit in the primary income balance. This is due to increased payments for returns on foreign direct investment. In addition, we expect increased payments for foreign portfolio investment. This is in line with improving domestic economic conditions and investor optimism. Therefore, we expect the current account deficit to widen further from -0.5 % of GDP in 2023F to -0.8 % of GDP in 2024F.

Exhibit 16: Oil price

Source: Bloomberg

Exhibit 17: Total import and import growth

Source: BPS

- Fiscal 2024 budget: Optimism, challenges, and the fiscal deficit target

The government and the DPR (People's Consultative Assembly) have set a fiscal deficit target of -2.3% of GDP for the 2024 State Budget (APBN). With estimated state revenue at Rp2,781.3 tn and state expenditures projected to reach Rp3,304.1 tn in 2024, we are optimistic about achieving the fiscal deficit target. This optimism is bolstered by the higher economic growth forecasted at 5.2% YoY for 2024, which we expect to increase tax revenue due to rising household consumption. Additionally, downstreaming initiatives that stimulate investment and exports will contribute to higher state income. Furthermore, the government has enacted tax regulation harmonization (HPP) laws that have a positive impact on state revenue. However, the potential increase in oil prices in 2024 could strain the 2024 APBN deficit target. Moreover, the expected salary increase for civil servants in 2024 is likely to increase state expenditures. We also anticipate populist government policies in a political year, such as providing social assistance. Therefore, we anticipate a fiscal balance of -2.2% of GDP in 2024, slightly deeper than the predicted -2.1% of GDP for 2023. These fiscal balance projections are in line with the government’s target (see exhibit 18).

Exhibit 18: Composition of state budget

Source: Ministry of Finance

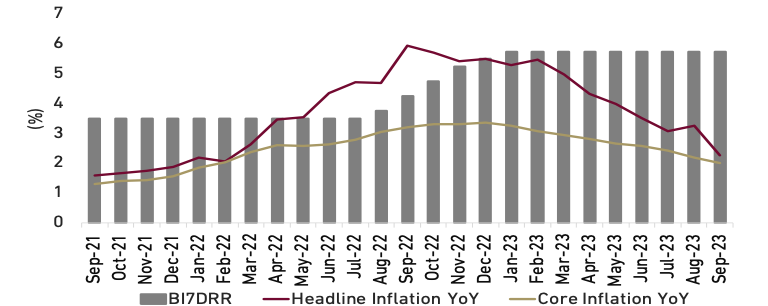

- El Niño's impact on rice supply: Challenges and strategies for indonesia's inflation management in 2024

According to the Indonesian Meteorological, Climatological, and Geophysical Agency (BMKG), an El Niño-like long dry season is currently expected to continue until February or March 2024. In response to this phenomenon, India as the largest rice producer in the world has imposed a ban on rice exports to ensure an adequate domestic rice supply. Concerns regarding rice supplies and food inflation may persist further influencing the Indonesian economy in next year. This situation could potentially lead the Indonesian government to continue competing with other rice-importing countries, especially if the drier weather begins to affect domestic production. Fortunately, the Indonesian government appears to be leading the way in securing global rice supplies. For example, they have recently doubled their rice import agreement with Cambodia to 250,000 tons per year for four years. This move is expected to fulfill approximately 35.6% of Indonesia's annual rice import target for 2023. The government has successfully maintained the inflation rate. In September, the headline inflation rate eased to 2.28% YoY, marking the fifth consecutive month within the target range of 2%–4% (see exhibit 19 for the inflation rate trend).We see that the inflation rate could be managed well in 2024 in line with the government's efforts to maintain and control food prices, both in terms of production, import, and distribution. Overall, we expect that the inflation rate will ease to 3.0% YoY in 2024, compared to our projection of 3.2% YoY for this year.

Exhibit 19: Inflation rate and BI7DRRR

Source: BPS and BI

- Interest rate outlook and implications for the rupiah

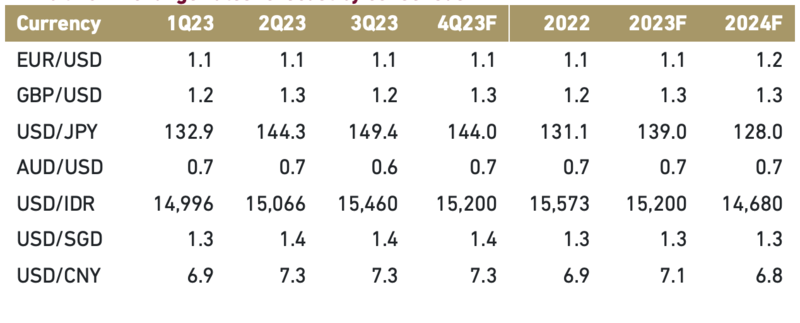

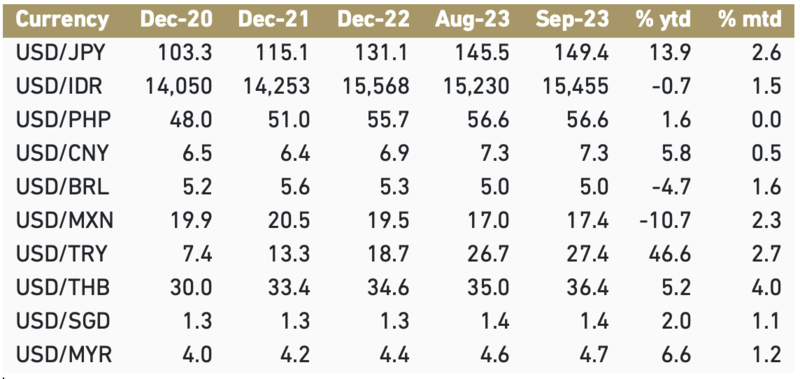

We expect 2024 to be a year in which the majority of central banks cut interest rates. This is mainly due to falling inflation and concerns about slowing economic growth as a result of high interest rates. Both the Bank of England (BoE) and the Swiss National Bank (SNB) have recently ended their rate hike cycles due to concerns about an economic slowdown. Meanwhile, the European Central Bank's (ECB) recent rate hikes are widely seen as the last in this cycle. The Federal Reserve (Fed) is also expected to taper in 2024, with an expected rate of 4.25%, in line with market expectations and consensus (see charts 4 & 7). The dovish stance is expected to ease pressure on the rupiah, and we are more optimistic that the exchange rate will reach Rp14,782/USD by the end of 2024, slightly higher than consensus estimates of Rp14,680/USD (see Exhibit 20), but stronger than our forecast for this year of Rp15,310/USD. Meanwhile, the rupiah has appreciated 0.73% YTD to Rp15,455/USD, outperforming the Philippine peso, Malaysian ringgit and Thai baht (see chart 21). Moreover, we believe that the government has effectively addressed inflation rates and will intervene in the foreign exchange and bond markets to maintain rupiah stability. Overall, we expect the BI rate (BI7DRRR) to decline to 5.00% in 2024, lower than the 6.00% forecast for 2023.

Exhibit 20: Exchange rates forecast by consensus

Source: Bloomberg

Exhibit 21: Global currencies

Source: Bloomberg

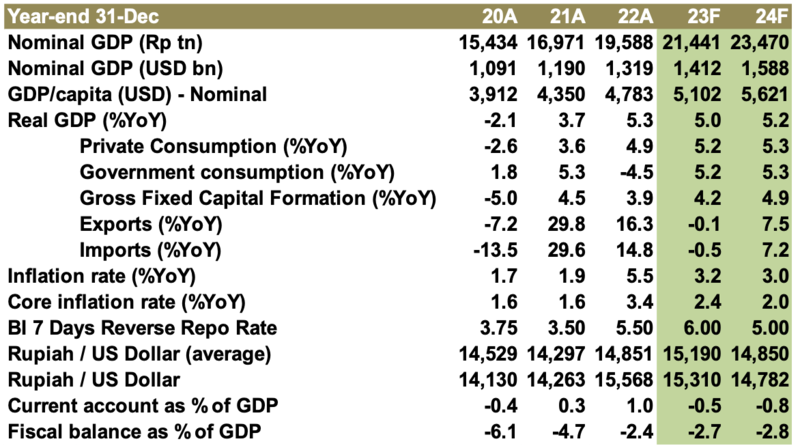

Exhibit 22: Macroeconomic Indicator

Source: BI, BPS, MoF and Ciptadana Estimates