Healthcare

Overweight

Sector Outlook

• Growth again outpaces GDP growth

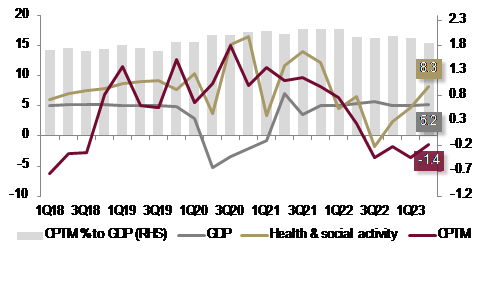

In terms of consumption, the Health and Social Activity component of GDP continues to attract attention, growing 8.3% YoY in 2Q23, coupled with a lower healthcare inflation rate. This suggests that households are still prioritizing health maintenance. On the other hand, the contribution of the chemical, pharmaceutical, and traditional medicine (CPTM) industry to GDP has been declining based on industry data, especially in 2Q22, reflecting the normalization after the pandemic. In 2Q23, these industries contributed 1.9% to GDP, experiencing a 1.4% YoY contraction, which persists due to the high base effect.

• Fiscal priority on health sector

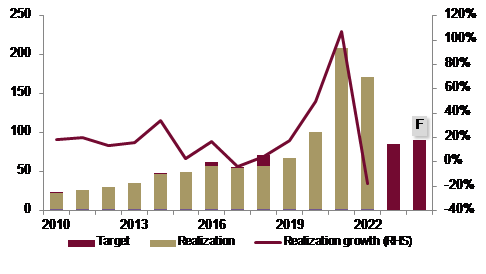

The health budget for 2024 is 5.6% of the state budget (APBN) or Rp186.4 tn, which is 8.1% higher than the APBN forecast for 2023. The allocation details include Rp107.2 tn for ministries/agencies (K/L), Rp14.2 tn for non-K/L expenditures, and Rp66.1 tn for regional transfers (TKD). The health budget allocation aims to achieve several objectives. First, it aims to reduce the prevalence of stunting from 21.6% in 2022 to 14% next year. In addition, the budget supports transformative primary services, such as treatment and care for pregnant women with chronic malnutrition, which contribute to stunting reduction. It also focuses on improving referral services to ensure equitable access to priority services for diseases such as heart, cancer and kidney. It also promotes national self-sufficiency in health care by encouraging domestic production of medical equipment and ensuring procurement. The transformation of the healthcare financing system will include incentives for healthcare professionals and the expansion of service coverage for the public under the National Health Insurance Scheme (JKN). Finally, the government will accelerate the transformation of healthcare technology.

Exhibit 114: GDP growth from health & social activity and pharmaceuticals (%)

Source: Bloomberg, Statistics Indonesia, Ciptadana Sekuritas Asia

CPTM: Chemicals, Pharmaceuticals, and Traditional Medicines

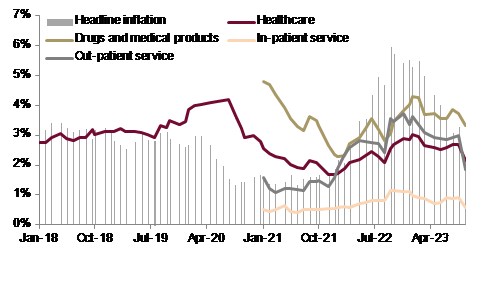

Exhibit 115: Inflation rate from healthcare and drugs & medical devices

Source: Bank Indonesia, Ciptadana Sekuritas Asia

P.S.: Out-patient service, in-patient service, and drugs & medical products are only available since 2021

• Above 5% to GDP despite of the removal of mandatory spending

After President Jokowi announced the 2024 State Budget (APBN), a spotlight has been cast on the Health Law since the law had initially sparked controversies, notably concerning the removal of mandatory spending on the healthcare sector, previously 5% of APBN. Many people are concerned that this elimination undermines legal certainty, posing a risk to the government's commitment to offering quality, accessible, and sustainable healthcare services. Things are getting crystal clear where the 2024 healthcare budget is set at 5.6% of the APBN. In the future, the health budget will align with the health sector's master plan through performance-based budgeting, addressing the previous lack of direction and planning. Historical inefficiencies, where funds were allocated without clear strategies, are being rectified. Reforms, including adjustments in Indonesia Case Based Groups (INA-CBG) tariffs and a more defined Coordination of Benefit (CoB) scheme, alongside the standardization of Social Security Agency on Health (BPJS Kesehatan) inpatient classes (KRIS) by Jul-25, instil optimism for the future. Thus, the health law, are expected to reshape Indonesia's healthcare sector significantly.

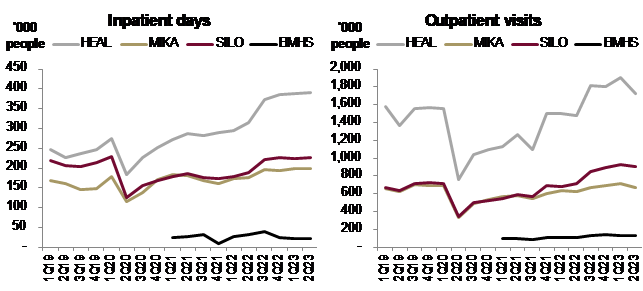

• Hospitals experienced traffic recovery post-pandemic

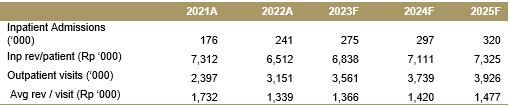

The evidence of increased healthcare demand is clearly demonstrated by the rising patient traffic within our hospital players. In fact, patient volume in major listed hospitals in Indonesia, namely HEAL, MIKA, and SILO, has surpassed pre-pandemic levels and grew by 3-years CAGR of 8/5% in 2019-2023F for inpatient days/outpatient visit, respectively. We believe this trend will persist in 2024F, driven by a growing demand for healthcare services. We believe that households have become more health-conscious in the post pandemic era. Moreover, the air pollution issue still prevails and the handling necessitates a lengthy period, also increasing the healthcare attention to some extent.

Exhibit 116: Ministry of Health budget and realization (in Rp bn)

Source: Bloomberg, Statistics Indonesia, Ciptadana Sekuritas Asia

Exhibit 117: Post-pandemic traffic recovery: SILO as the best performer

Source : Companies and Ciptadana Sekuritas Asia

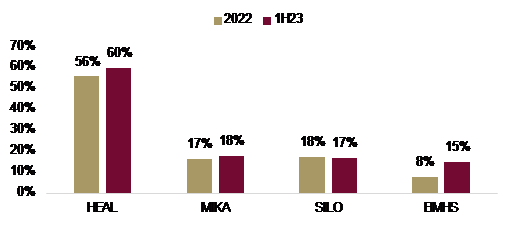

• More and more attractive JKN service for hospital players

After the hike of INA-CBG tariffs in early 2023, JKN services have became more attractive to hospitals operators. The capitation rates have become higher and more reasonable for doctors, leading many hospitals to target increased exposure to JKN services. Currently, HEAL is the largest beneficiary of this trend, with 60% of its revenue coming from JKN services. Other hospitals, including MIKA and BMHS, also aim to increase their exposure to JKN, resulting in a larger JKN revenue contribution in 1H23 as compared to 2022. Even SILO, which primarily focuses on the premium segment, continues to provide services to BPJS patients, with 18 out of their total 41 hospitals primarily catering to this segment.

• Expecting realization of CoB at the latest by completion of KRIS implementation

Further catalyst for JKN play will come from a clearer implementation of Coordination of Benefit (CoB) scheme following Ministry of Health Regulation No.3 of 2023. The CoB scheme will provide an upside to JKN’s margin given its coordination scheme between BPJS and private insurances. This collaboration also will benefit the industry by sharing burdens between government and private, making healthcare more accessible.

JKN services also will subject to Standardized Inpatient Class (KRIS), with completion targeted by 2025. The tariff rates in KRIS will also be standardized, but the uniformed tariff will be determined after the revision of Presidential Regulation 82/2018 concerning Health Insurance is finalized. KRIS scheme will standardize room facilities and amenities for inpatient treatments. It is expected that implementation of CoB could be taken at the latest along with the full implementation of KRIS. This is to prevent the potential decrease in the level of service for participants who were previously in JKN Class 1 program, which mainly consists of Wage Workers (Pekerja Penerima Upah or PPU) segment. With the implementation CoB, a solution will be available for both workers and employers to maintain the standard level of service they currently receive.

Exhibit 118: JKN contribution to total revenue

Source : Companies and Ciptadana Sekuritas Asia

• Awaiting for implementing regulation of Health Law

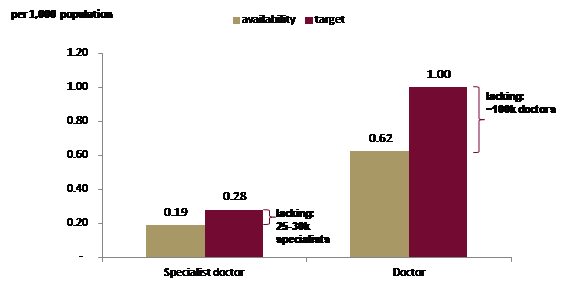

We expect the Law No.17 of 2023 (or the Health Law) will bring structural reform, flourishing the healthcare industry. Currently the health law is still awaiting for the derivative regulations, with 108 article is scheduled to be delegated to be regulated by Government Regulations (totaling 101 articles), Presidential Regulations (2 articles), and Minister of Health Regulations (5 articles). We believe more implementation will bring brighter prospects for both pharmacy and hospital players.

Hospitals will benefit in the short and longer term through: 1) the improved availability of medical talents across regions in Indonesia; 2) the offering of more complex cases locally with the entrance of highly skilled-diaspora and foreign doctors; and, in the longer term 3) larger local medical tourism instead of overseas medical visits, leading to 4) more potential for hospital expansion outside big cities following the availability of medical talents. We believe SILO is well positioned to benefit from this, given its focus on premium segment and its reputation for attracting medical talents. The health law will also benefit those hospitals with strong focus on centre of excellence, such as oncology, neurology, cardiology, fertility, urology, etc.

• Smaller hospital addition to improve occupancy

Hospital players will continue to focus on improving bed occupancy rates in existing hospitals and performing only a selective new hospitals expansion. In the past, hospitals has expanded quite aggressively at >5% new hospitals annually in the 2012-2017 period and 2-3% annually in 2018-2022 period. We expect the trend of new hospital acquisitions to remain moderate in 2024. There is also a trend toward larger acquisition through managed service hospitals, as it requires lower capex.

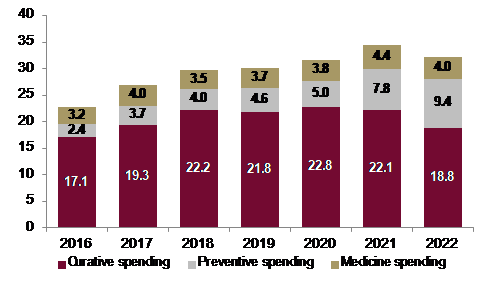

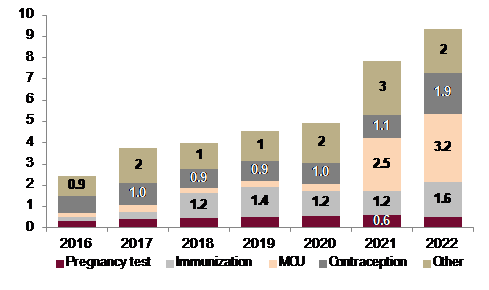

• Higher awareness on preventing disease

Indonesians spend an average of Rp32,168/month on healthcare. Notably, spending on preventive measures has risen to 29% of total monthly healthcare expenditure, highlighting a growing awareness of prevention. Medical Check-Ups (MCU) constitute 34% of preventive spending, a substantial increase from previous years, indicating proactive health monitoring. Other components such as fitness, massage, vitamins, and herbs show a trend of preventative actions. This favourable trend should benefit healthcare industries.

Exhibit 119: Health Law to fulfill the gap of medical talents faster

Source : MoH, WHO, and Ciptadana Sekuritas Asia

Exhibit 120: Monthly healthcare expenditure/capita (in Rp thousand)

Source: Statistics Indonesia, Ciptadana Sekuritas Asia

Exhibit 121: Monthly preventive spending/capita (in Rp thousand)

Source: Statistics Indonesia, Ciptadana Sekuritas Asia

• Telemedicine: as a complement to conventional health treatments

The rise telehealth will serve as an entry point for customers to access in-person health services, rather than being a threat to the industry, in our view. We expect further digital collaborations between the telemedicine, hospitals, and pharmaceutical industries will be more common ahead. This should be positive for all involved entity, resulting in a positive ripple effect that boosts demand for healthcare products and services.

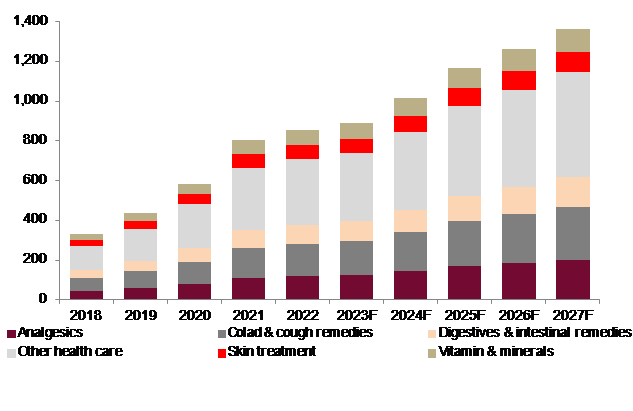

• Growing pharmaceuticals market

According to Statista, the pharmaceuticals and cosmetics market in Indonesia is expected to witness significant growth, with projected revenues reaching USD1 tn in 2024 and an estimated CAGR 2023-2027 of 11.3%. Notably, China is poised to be a major revenue generator, with a projected market volume of USD 19 tn in 2023. This market is expected to have 58.6 million users by 2027, with user penetration expected to increase from 15.3% in 2023 to 20.5% in 2027. Furthermore, the average revenue per user (ARPU) is projected to be USD 20.9 or around Rp323,950, indicating a promising revenue potential in the coming years. We expect the same thing to happen in Indonesia as health awareness grows.

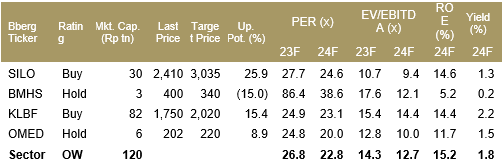

• Overweight rating for healthcare sector, with SILO as our top picks.

We maintain our Overweight rating on the healthcare sector as we believe the sector remains a promising long-term prospect in Indonesia. We expect the sector to be positively impacted by healthier regulations and healthcare reform, which will manifest in both the short and long term, providing numerous catalysts along the way. SILO is our top pick among the hospital and pharmacy players. We like SILO for its stronger-than-peer recovery in patient traffic and how the company will benefit from the improved healthcare sector in Indonesia over the long term.

Exhibit 122: Estimated revenue in pharmaceuticals industry (in USD mn)

Source: Statista, Ciptadana Sekuritas Asia

Exhibit 123: Healthcare stocks rating and valuation

Source: Bloomberg, Ciptadana Sekuritas Asia

Erni Marsella Siahaan, CFA +62 21 2557 4800 ext. 919 [email protected]

Nicko Yosafat +62 21 2557 4800 ext. 760 [email protected]

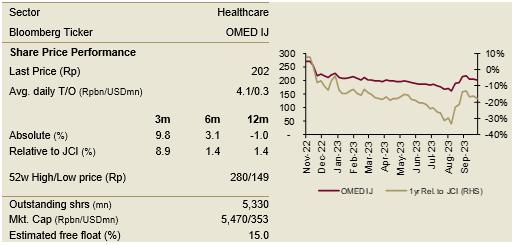

Jayamas Medica Industri

HOLD TP: Rp220 (+8.9%)

Company Profile

PT Jayamas Medica Industri (OMED) was established on December 15, 2000 and commenced operations in 2002. OMED and its subsidiaries are mainly engaged in manufacturing, distribution and retail of medical supplies and equipment. OMED produces a wide range of medical supplies and equipment from medical gloves, syringes and needles to hospital furniture.

Key Points

• Rising demand amid pollution issues and heightened health awareness. Currently, Indonesia faces severe air pollution, ranking highest globally in the air quality index according to IQAir. This crisis has led to a surge in acute respiratory infections (ISPA) cases, making ISPA reaches top 5 causes of health claim in 2022. OMED stands to benefit greatly. The pressing needs to combat air pollution and higher hospital claims can boost demand significantly for OMED's products.

• Expanding customer base. In the 2Q23, OMED experienced significant growth in its customer base, particularly from government entities, which increased by 77.3% QoQ. This demonstrates OMED's growing credibility and trust, especially among public institutions. With a diverse customer base spanning distributors, hospitals, clinics, laboratories, retail and government entities, OMED is on a trajectory of increasing demand.

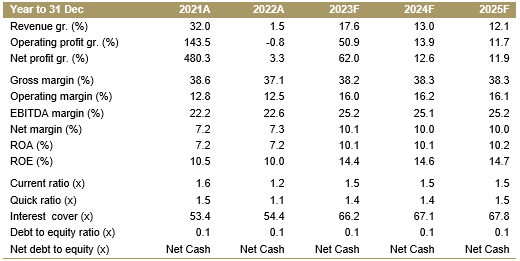

• Hold rating for OMED with 2024F TP of Rp220. - Hold rating on OMED with 2024F TP of Rp220. With Rp645.8 bn of idle funds, OMED is well-positioned for strategic investments and expansions to ensure sustainable growth. With only 8.9% upside potential, we have a Hold rating on OMED with a 2024F TP of Rp220/sh, derived from a 2024F PER of 20.9x at +1 std dev FY24F. Risks to our call: lack of public awareness of air pollution, stiff competition

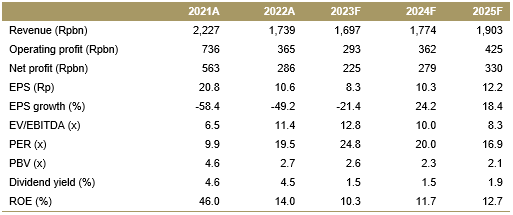

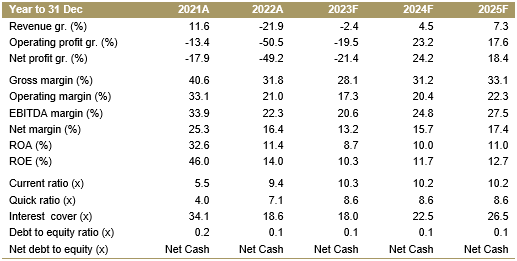

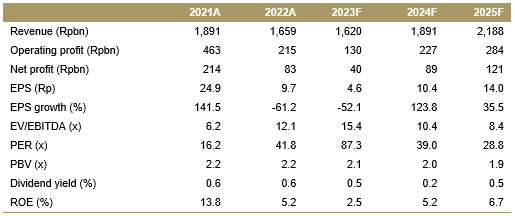

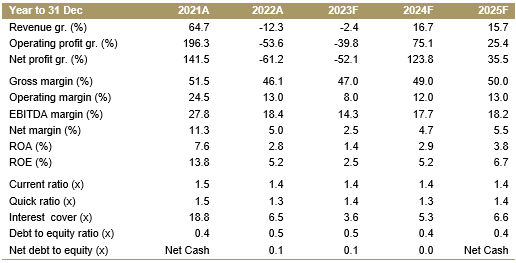

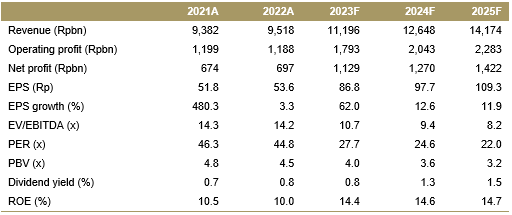

Financial Highlights

Assumptions

Nicko Yosafat +62 21 2557 4800 ext.760 [email protected]

Jayamas Medica Industri

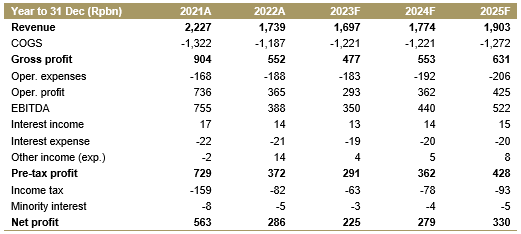

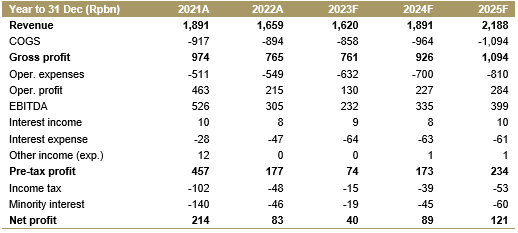

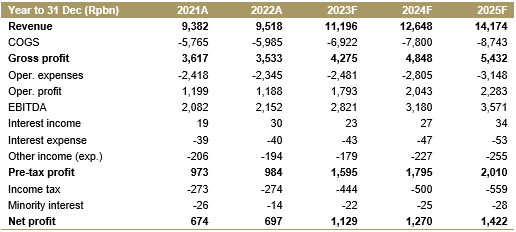

Income Statement

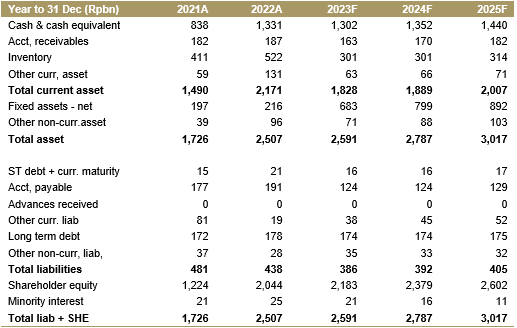

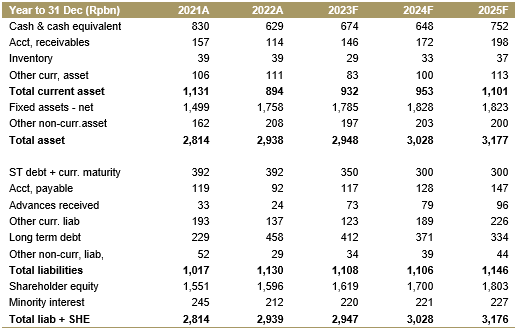

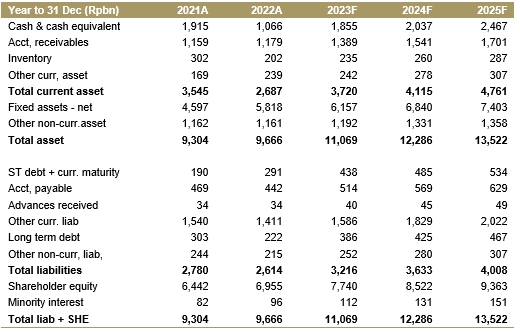

Balance Sheet

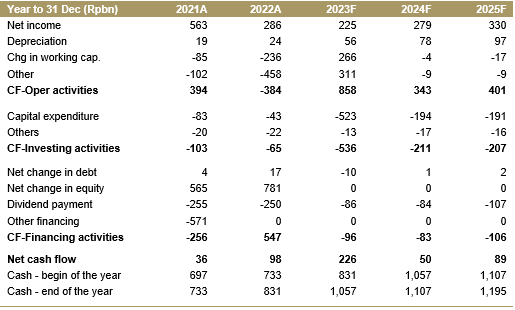

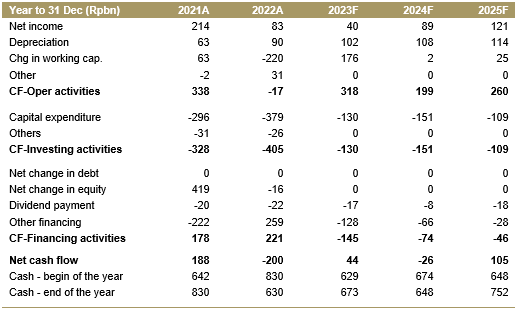

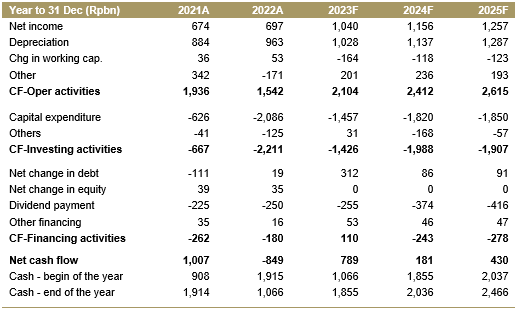

Cash Flow

Key Ratios

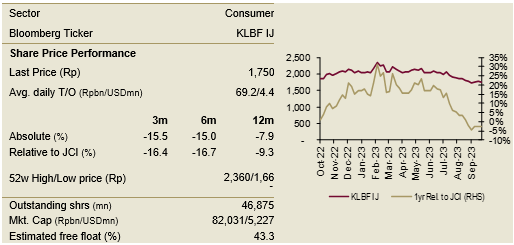

Kalbe Farma

BUY TP: Rp2,020 (+15.4%)

Company Profile

Kalbe Farma (KLBF), established in 1966, is one of the largest listed pharmaceutical companies in Southeast Asia. It operates four divisions, namely Prescription Pharma (licensed, unbranded and branded generic drugs), Consumer Health (OTC drugs and energy drinks), Nutritionals-based on milk powder, and Distribution and Logistics divisions.

Key Points

• Never stop innovating. KLBF expects the Indonesian Food and Drug Administration (BPOM) to approve HLX10 and GX-E4 for small cell lung cancer in 1Q24. Both are critical to KLBF's goal of doubling specialty product sales by 2024. In addition, KLBF is forming a joint venture with PT Tri Investama Solusindo, a leading cold chain company. This partnership, which will commence in 4Q23, will strengthen the distribution and logistics segment in 2024.

• Margin improvement ahead. We expect the gross profit margin (GPM) to improve to 42.7% (vs. 40.5% in FY22) due to the declining price of skim milk powder and the new health law, which could increase sales of licensed and branded drugs with higher GPMs. However, one of the biggest challenges is the depreciation of the exchange rate, but our economist estimates that the exchange rate could appreciate to Rp14,782 by YE24.

• Maintain BUY rating on KLBF with 2024F TP of Rp2,020. Story about Sanofi and KlikDokter also solidifies KLBF's performance. We like KLBF as health awareness is getting higher these days. We have BUY rating on KLBF with 2024F TP of Rp2,020/sh, derived from 2024F PER of 26.5x e. Risks to our call: prolonged rupiah depreciation, cancellation of ongoing joint ventures.

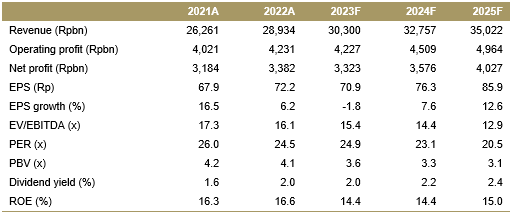

Financial Highlights

Assumptions

Nicko Yosafat +62 21 2557 4800 ext.760 [email protected]

Kalbe

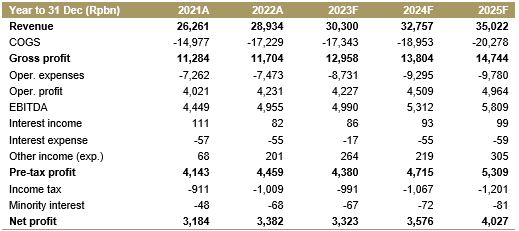

Income Statement

Balance Sheet

Cash Flow

Key Ratios

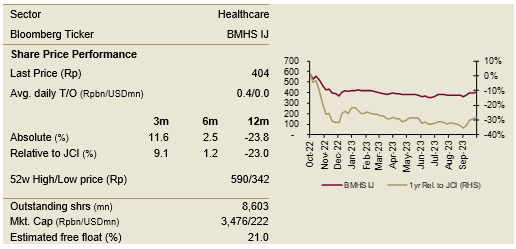

Bundamedik

HOLD TP: Rp340 (-15.8%)

Company Profile

Established in 1973, Bundamedik (BMHS) is one of the Indonesia’s leading health care service providers with strong track record and expertise in premium women and children segment. BMHS has strong brand equity which allows it to grab new patients and increase its existing patient’s loyalty. The company also has Morula as market leader in In-Vitro Fertilization (IVF) market and Diagnos as it lab-test based arm.

Key Points

• We believe BMHS mother and child segment to remain the strongest contributors to BMHS, as the company have strong brand equity and reputable in mother and child segment. We believe this will support BMHS gross margins, as BMHS holds the premium mother and child services. However, mother and child segment as the most lucrative segment is also now being targeted by major hospitals in Indonesia, creating a stronger competition in 2024F.

• Heavier competition also will persist on In vitro fertilisation (IVF) services. Morula (IVF) traffic saw a deeper slowdown compared to the hospital traffic, with number of cycle declined by -17% QoQ in 2Q23 and cumulatively by -10% YoY in 1H23. Despite the slowing traffic trend in the past several quarters, we believe BMHS will retain its position as market leader in IVF (currently with 45-47% market share) banking on it value proposition on PGT-A testing.

• BMHS has succeeded to enlarge its exposure on JKN by raising the segment’s contribution to 15% in 1H23 from 8% in 2022. This is as a step to benefit more from the more favourable JKN scheme.

• Maintain Hold with TP of Rp340/share, based on 9x target EV/EBITDA 2024F, which lower than local hospital players avg. at 15x considering its below peers performance. The stock is currently traded at 10x EV/EBITDA 20224F.

Financial Highlights

Assumptions

Erni Marsella Siahaan, CFA +62 21 2557 4800 ext. 919 [email protected]

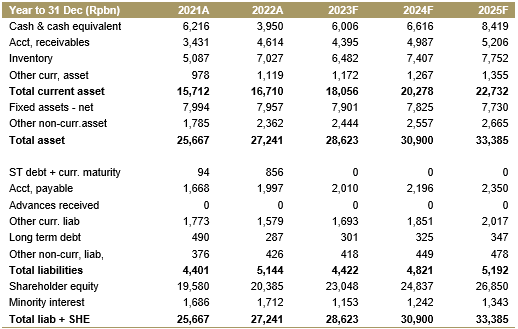

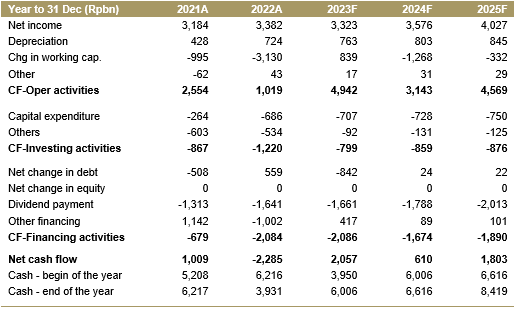

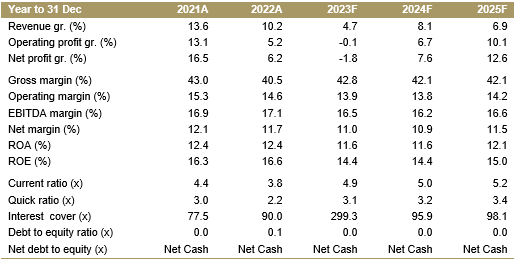

Bundamedik

Income Statement

Balance Sheet

Cash Flow

Key Ratios

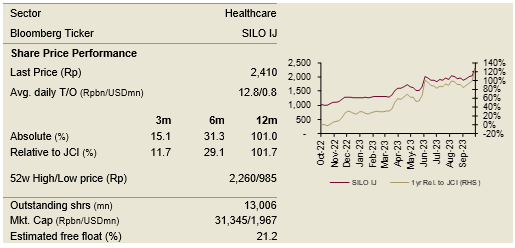

Siloam Hospitals

BUY TP: Rp3,035 (+25.9%)

Company Profile

Established in 1996, Siloam Hospitals (SILO), which is subsidiary of LPKR property developers in Indonesia, offers valuable service for coverage expansion from the onset of JKN. SILO operates 41 hospitals of varying degree of profitability in 23 provinces throughout the country, and 4k bed capacity supported by ~3,800 specialists and general practitioners and >8k nurses and support staff. Main focus of the company remained to be private payers (83% of revenue) followed by BPJS (17% of revenue).

Key Points

• SILO has experienced a stronger rebound in patient traffic compared to its peers post-pandemic. This resulted in a consistent EBITDA margin of 29-30% in the last four quarters, which will still improve going forward.

• The room for further EBITDA improvement for SILO remained open given: 1) company focus on the top craft groups which consistently being the growth machine, 2) company focus on high intensity cases resulting in higher margin, 3) larger digital processing and digital channels for customers, and 4) improving economies of scales along with growing traffic.

• The company remained focus on premium hospitals with greater cases complexity. Hence we see the new Health Law implementation will benefit SILO as they are in a good position on attracting medical talents. They also remained to set 18 out of their 41 total hospitals to serves mainly BPJS patients with narrower range of service. Given this clear focus classification among its hospitals, the company will remain focus on existing hospital and remain selective in new hospital expansions.

• SILO is our top pick among the hospital players (TP: Rp2,565/share). We think the stock is worth of re-rating and currently still has undemanding valuation of 8.2x 12-month forward EV/EBITDA, below its historical trading average of 12x.

Financial Highlights

Assumptions

Erni Marsella Siahaan, CFA +62 21 2557 4800 ext. 919 [email protected]

Siloam Hospitals

Income Statement

Balance Sheet

Cash Flow

Key Ratios