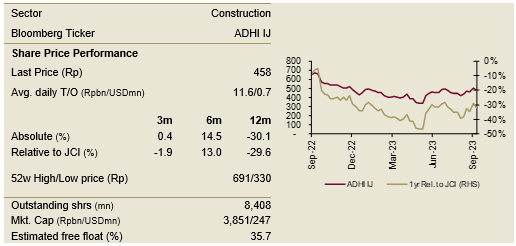

Construction

Underweight

Sector Outlook

• Ballooning debt problem brings long-term uncertain prospects

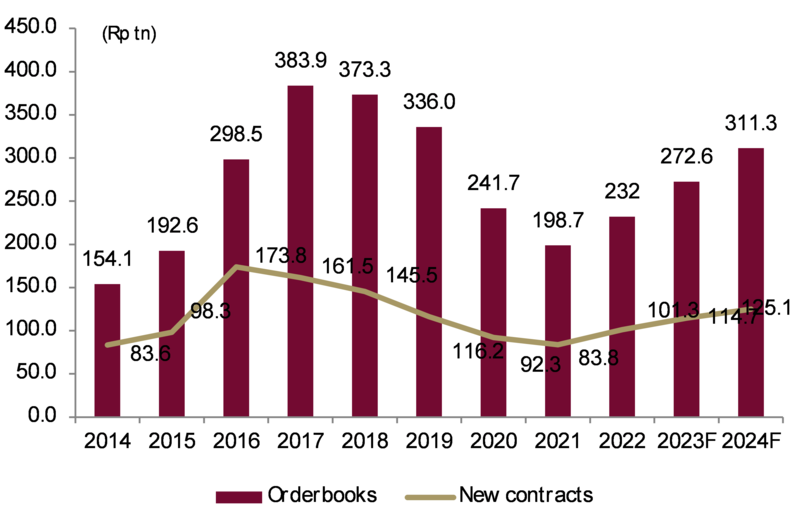

The government has been relying on massive infrastructure to achieve ambitious GDP growth target since President Jokowi took office in 2014. The country needs better transport links such as railways, airports, toll roads as well as energy supplies, and such projects promise long-term economic benefits. Aggressive expansion of infrastructure to drive economic growth has saddled the country's four largest listed construction companies (WIKA, PTPP, WSKT, and ADHI) with very high debt levels due to high working capital requirements from massive and rapid order book growth, which more than doubles between 2014 to 2019. Since the contractors have incurred the up-front costs and sometime the equity participation of taking on the government contracts, it requires them to tie up trillion of rupiah in working capital. Often, contractors don’t get paid until projects are 100% completed under turnkey projects.

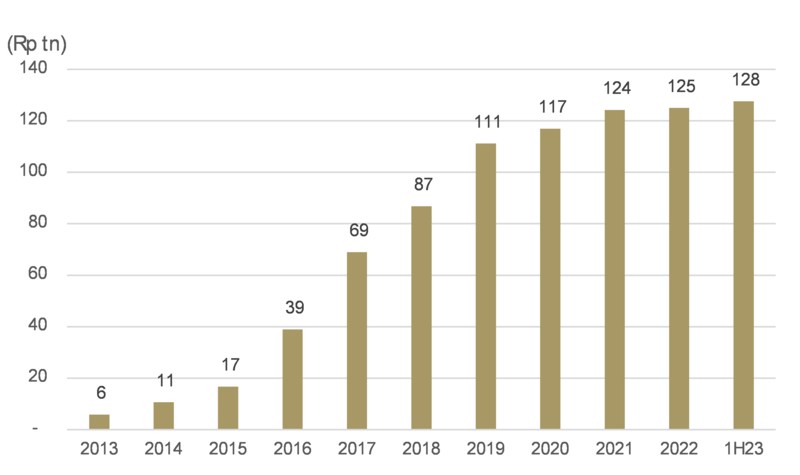

This forced them to massive debt resulting in total debt among them of nearly Rp128 tn by end-June 2023, a 12-fold increase from less than Rp11 tn in 2014. They are now struggling to repay, with WSKT and WIKA asking seek a payment delay from its bondholders and creditors while PTPP and ADHI’s subsidiaries being sued by several customers over the Postponement of Debt Payment Obligation (PKPU) case. The SOE contractor’s debt issue has caused jitters in the stock market after WSKT defaulted on several bonds and WIKA proposed a moratorium on bank debt payments this year. We believe bond holders of WSKT and WIKA can only sell their portfolio at a significant discount. We also suspect that state pension funds' money is trapped in WSKT and WIKA bonds because they cannot sell them if they incur losses, The Ministry of State-Owned Enterprises has tried to save WSKT by forcing state banks to agree to the company's 10-year restructuring plan, but private bondholders have rejected the plan. This creates long-term uncertainty for the sector.

Exhibit 172 : SOE contractors orderbooks and new contracts

Source: Company and Ciptadana estimates

Exhibit 173 : SOE contractors total debt

Source: Company and Ciptadana estimates

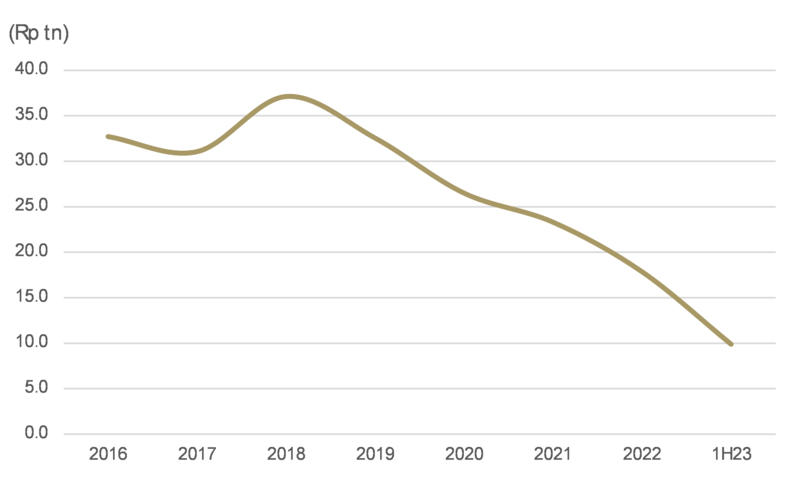

• Significant decline in cash balances due to financing issues

The high level of debt will limit the ability of SOE contractors to raise funds from local banks and the domestic bond market, as the Ministry of State Enterprises plans to restrict the disbursement of loans from state-owned banks to indebted SOE contractors, amid concerns about their ability to repay. This, in our view, has forced SOE contractors to use more internal cash to procure raw materials for projects and meet day-to-day needs.

We see the total cash balance of all SOE contractors dropping significantly by 45% from Rp17.9 tn at the end of 2022 to only Rp9.9 tn at the end of Jun-23, with WIKA and PTPP recording the highest decline of 68% and 49% to Rp1.8 tn and Rp2.8 tn, respectively. We are concerned that if this problem continues for a longer period of time, it may lead to the stalling of projects.

Exhibit 174 : SOE contractors cash balance

Source: Company

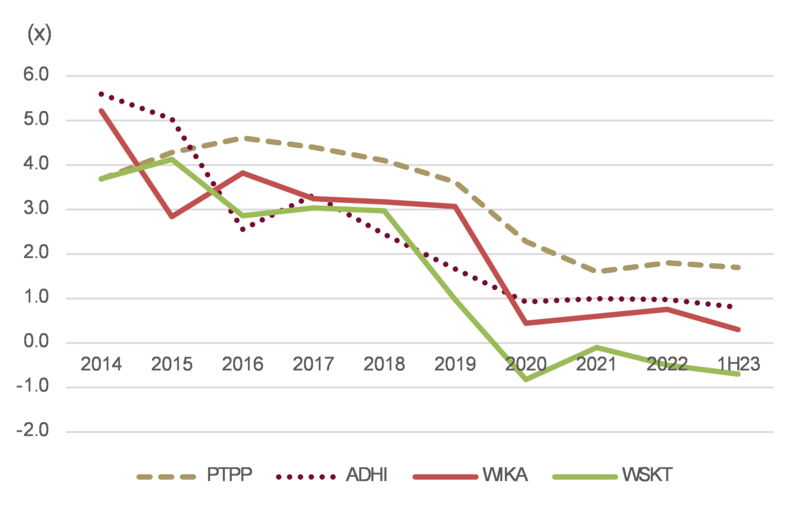

• High interest expenses significantly dent contractors’ profitability

Highly leveraged contractors also continue to suffer from low profitability as tight working capital has led to slow project execution. This has eroded their profit margins. The poor financial performance was further weighed down by high interest expenses on accumulated debt; they had already experienced a significant decline in their interest coverage following the Covid situation and ballooning debt. Their interest coverage ratio, which is defined as the ratio of a company's operating income to its interest expense, has declined significantly from an average of 4.5x in 2014 to 0.7x in 2020 and 0.5x at the end of June 2023. PTPP stands out with a still high interest coverage ratio of 2.3x in 2020 and 1.7x in 2023 compared to ADHI's 0.9-0.8x, WIKA's 0.4x-0.3x and WSKT's negative coverage ratio due to negative operating profit since 2020. As their operating profit cannot cover the cost of interest expense, WSKT and WIKA have turned net loss since 2020 and 2022, respectively.

Exhibit 175 : SOE contractors interest coverage ratio

Source: Company

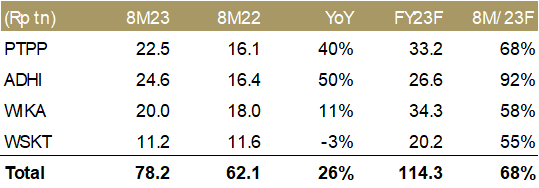

• New contracts grow strongly but do not generate significant profits

Aggregate contractors' new contracts grew by 26% YoY to Rp78.2 tn in 8M23, with ADHI posting the highest growth of 50% YoY to Rp24.6 tn, which is also the highest contract value in the sector and reached 92% of our 2023F. During the period, ADHI secured Rp6.8 tn of new contracts from MRT Jakarta Phase 2 and Rp3.7 tn from the LRT project in the Philippines. This is followed by PTPP which secured Rp22.5 tn of new contracts, growing by 40% YoY and reaching 68% of our 2023F. WSKT was the only contractor to post negative contract growth of -3%, which we believe is due to a severe working capital issue hindering the company's ability to participate in tenders.

Exhibit 176 : 8M23 new contracts , growth and achievement to target

Source: Company and Ciptadana estimates

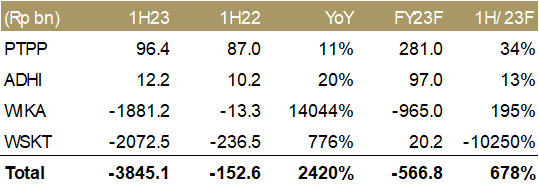

Despite growing new contracts, SOE contractors are posting relatively small profits at PTPP and ADHI and larger losses at WIKA and PTPP. We believe this is due to a combination of slower project execution resulting from tight working capital problem as well as high interest expenses. PTPP posted the highest profit of Rp96.4 bn (+11% YoY) and reached 34% of our 2023F. Despite posting the largest growth in new orders, ADHI only posted a small profit of Rp12.2 bn (+20% YoY) and met 13% of our 2023F. Meanwhile, WIKA and PTPP saw their net losses widen by 14x and 8x to Rp1.9tn and Rp2.1tn respectively.

Exhibit 177 : Contractors’ 1H23 net profit

Source: Company and Ciptadana estimates

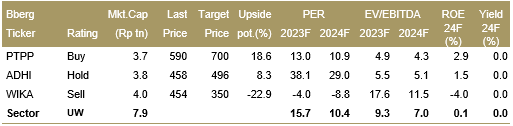

• Underweight on weak outlook and lingering debt problem

We underweight on the construction sector as subdued financial performance in 1H23 has kept construction stocks under pressure as they face various execution challenges and massive debt. Our net profit forecast for ADHI and PTPP in 2023F is only 15-30% of pre-covid levels and is expected to improve to 34-35% of pre-covid levels in 2025F. We believe that an important aspect of the contractor, is to maintain the right level of margin to cover costs and generate substantial profit. PTPP is the only SOE contractor that we expect to book sizable profit of above Rp250 bn compared to huge loss to be booked by WSKT and WIKA and small profit in ADHI. This is mainly helped by its ability to generate the highest gross margin of 14.2% vs average peers’ margin of 9.5% in 1H23. PTPP is our top pick in the construction space. We currently suspend our coverage on WSKT as we think the pathway to profitability in the near-to-medium term lacks visibility following heavy debt issues.

Exhibit 178: Construction sector rating and valuation

Arief Budiman +62 21 2557 4800 ext. 819 [email protected]

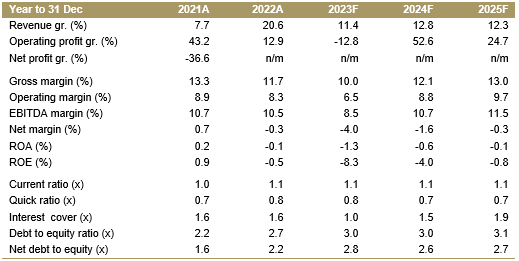

Adhi Karya

HOLD TP: Rp496 (+8.3%)

Company Profile

Adhi Karya (ADHI) is one of the largest SOE construction companies, providing construction services for civil works and EPC for power plants. The company also operates a real estate unit, including its own hotel, and an investment unit (precast concrete). In early 2017, ADHI signed the contract for the Jabodetabek LRT project phase worth Rp23.3 tn. Its subsidiary, Adhi Commuter Property (ADCP), which has a transit-oriented development (TOD) concept, is expected to see more positive sales in the high-rise residential segment after the LRT operation. ADHI is working on the construction of raw water supply infrastructure in Sepaku, North Penajam Paser Regency, which is part of the development of the New Capital City (IKN) Nusantar

Key Points

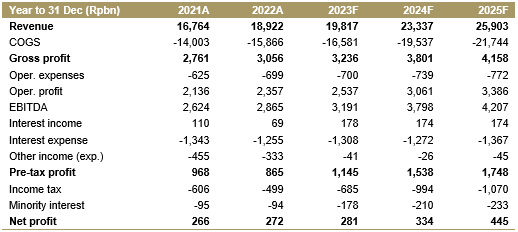

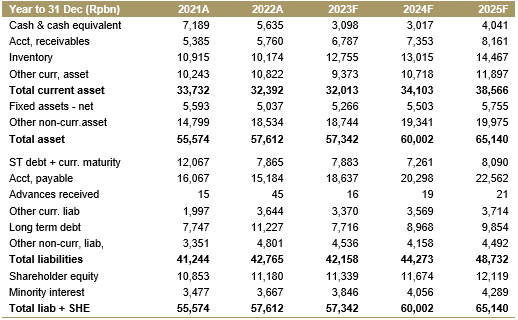

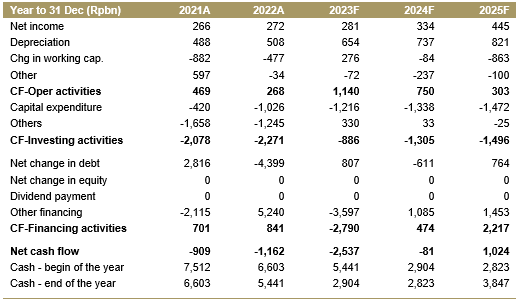

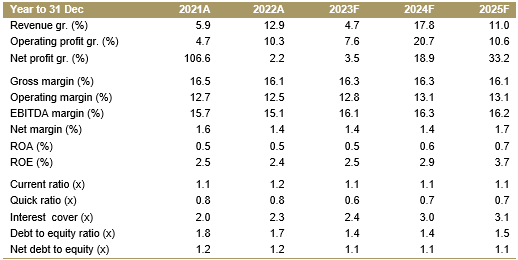

• ADHI’s new contracts are the highest among peers. The company has secured Rp24.6 tn (+50% YoY) new contracts in 8M23. This represents 79-92% of the company's internal and our 2023 guidance, which is higher than our expectations compared to historical performance of 65-72%. However, strong new contract growth has not yet supported revenue, which was flat YoY. We believe this was due to lower project execution, which was impacted by the stretched working capital issue.

• Largest cash balance in the sector. As of June 23, ADHI has Rp3.5 tn of cash on the balance sheet, the largest in the sector, which could be used for working capital and general purposes.

• Interest expenses ate up 78% of operating profit in 1H23. We are concerned the largest chunk of operating profit was used to cover interest expenses, leaving ADHI with very small of net profit Rp12.4 bn.

• We maintain Hold rating and TP Rp496 (limited upside of 8.3%). We suggest investors to wait for a better entry point as the expectation of prolonged debt overhang in the construction sector may continue to pose downside risk to our estimates.

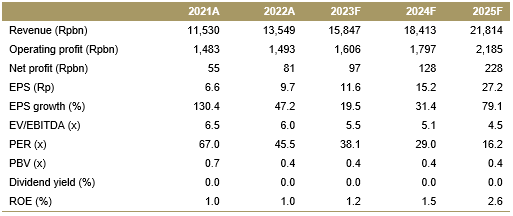

Financial Highlights

Assumptions

Arief Budiman +62 21 2557 4800 ext. 819 [email protected]

Adhi Karya

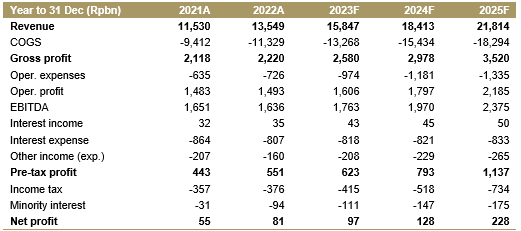

Income Statement

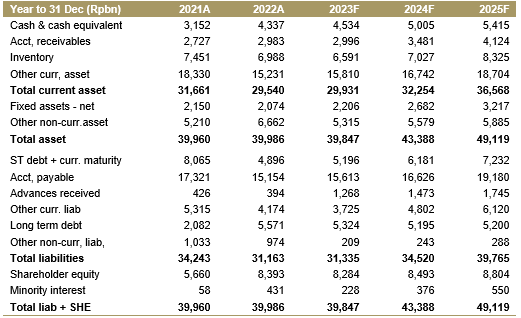

Balance Sheet

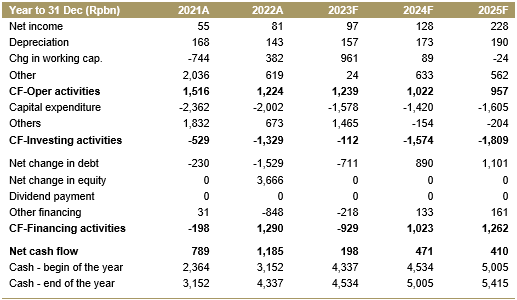

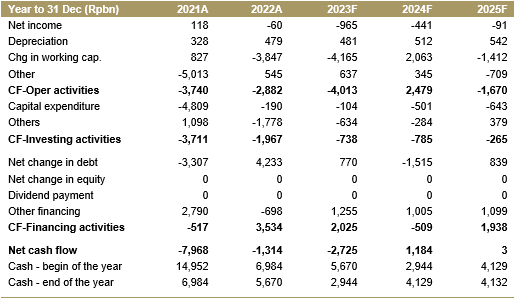

Cash Flow

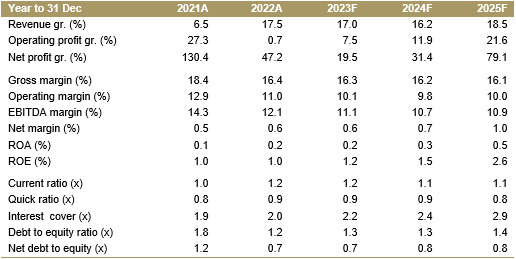

Key Ratios

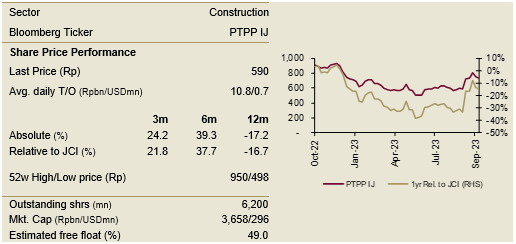

PT PP (Persero)

BUY TP: Rp700 (+18.6%)

Company Profile

Established in 1953, PTPP is one of the largest state-owned contractors. It offers construction services in civil works (including ports, roads, and bridges) as well as EPC segments. The company also runs property, realty, precast manufacturing and investment business. PTPP could benefit from its expertise in maritime construction its EPC expertise in oil and gas/mining projects which usually have higher margins. PTPP also has a stake in Batang Industrial Estate and leads construction process at the estate. As a contractor with the highest contract value for IKN in Rp22.6 tn within 2022 to Aug-23, PTPP will still be aggressively targeting new IKN projects in 2024 onwards.

Key Points

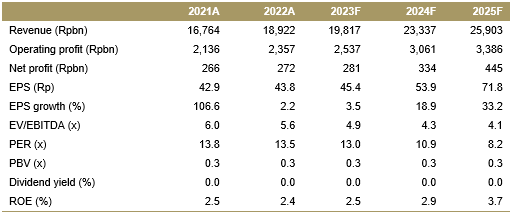

• The largest profit in the sector. 1H23 net profit rose by 11% YoY to Rp96.4 bn, mainly supported by 82% QoQ improvement in 2Q23 earnings due to seasonality, its net profit was the largest in the sector compared to ADHI's of Rp12.2 tn and huge loss at WIKA-WSKT of Rp1.9-2.1 tn, respectively.

• Delivering 40% growth in new contracts. PTPP obtained new contracts worth Rp22.5 tn (+40% YoY) in 8M23. PTPP is optimistic that this performance can continue to grow, reaching Rp34.5 tn in 2023.

• The government plans to merge PTPP and WIKA in 2024. We are neutral on the plan as the details are yet to be provided.

• Maintain Buy and TP of Rp700. We maintain our Buy rating on PTPP with TP of Rp700 based on 13.0x 2024F PER, which is in line with historical average. PTPP is our top pick in the sectors on its highest gross margin of 14.2% vs average peers of 9.5% in 1H23, which we believe is an important aspect of the contractor especially at current weak sector outlook. It has a cash balance of Rp2.9 tn at end of 2023 to support working capital, which is the second highest after ADHI’s Rp3.2 tn.

Financial Highlights

Assumptions

Arief Budiman +62 21 2557 4800 ext. 819 [email protected]

PT PP

Income Statement

Balance Sheet

Cash Flow

Key Ratios

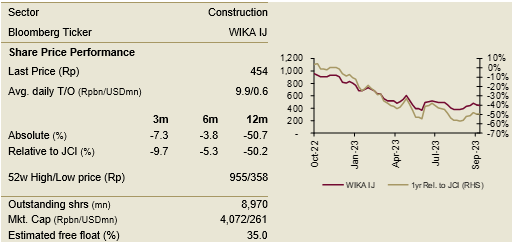

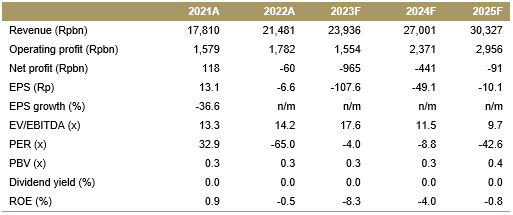

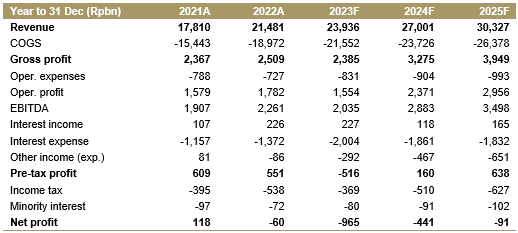

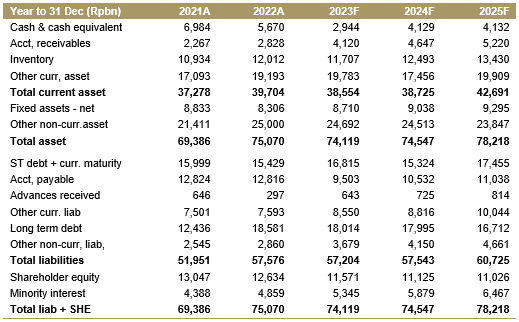

Wijaya Karya

SELL TP: Rp350 (-22.9%)

Company Profile

Wijaya Karya (WIKA) is the most diversified and second largest contractor by market-cap and order book in Indonesia. Its business segments are infrastructure & building, energy and industrial plant, industrial (precast and asphalt producer), realty and property as well as investment. WIKA was awarded the civil work contract of the Jakarta-Bandung high-speed railway (HSR) worth ~ Rp17 tn. HSR completion was delayed due to the Covid-19 pandemic and cost overruns due to design changes and delayed land clearing totalling Rp18 tn.

Key Points

• Government approved additional capital injection (PMN) of Rp6 tn in 2024. This will be used to strengthen WKA’s current projects financing capabilities. This will be used to strengthen WKA's ability to finance current projects. PMN will be followed by a rights issue. Judging by the recent rights issue of another SOE (WSKT and ADHI), we do not expect full participation from public shareholders given WIKA's current weak profitability.

• Refinancing risk increases. This is due to its recent standstill position to serve its bank obligations, more limited financial flexibility triggered by a weaker financial profile and negative market sentiment towards the construction sector.

• We are worried about WIKA cash balance of only Rp1.8 tn at end of Jun-23, down significantly from Rp5.7 tn at end of Dec-22. We believe the difficulty to get new loan has forced WIKA to use internals cash to procure raw materials for projects and to meet day-to-day requirements. Meanwhile, company’s DER rose from 1.9x in Dec-22 to 2.2x in Jun-23.

• We have Sell rating and TP of Rp350 on WIKA as we expect it continue posting net loss until 2025. Our TP is based on 2024F EV/EBITDA of 7.0x as WIKA

Financial Highlights

Assumptions

Arief Budiman +62 21 2557 4800 ext. 819 [email protected]

Wijaya Karya

Income Statement

Balance Sheet

Cash Flow

Key Ratios